The Bottleneck Has Moved — and Wall Street Just Noticed

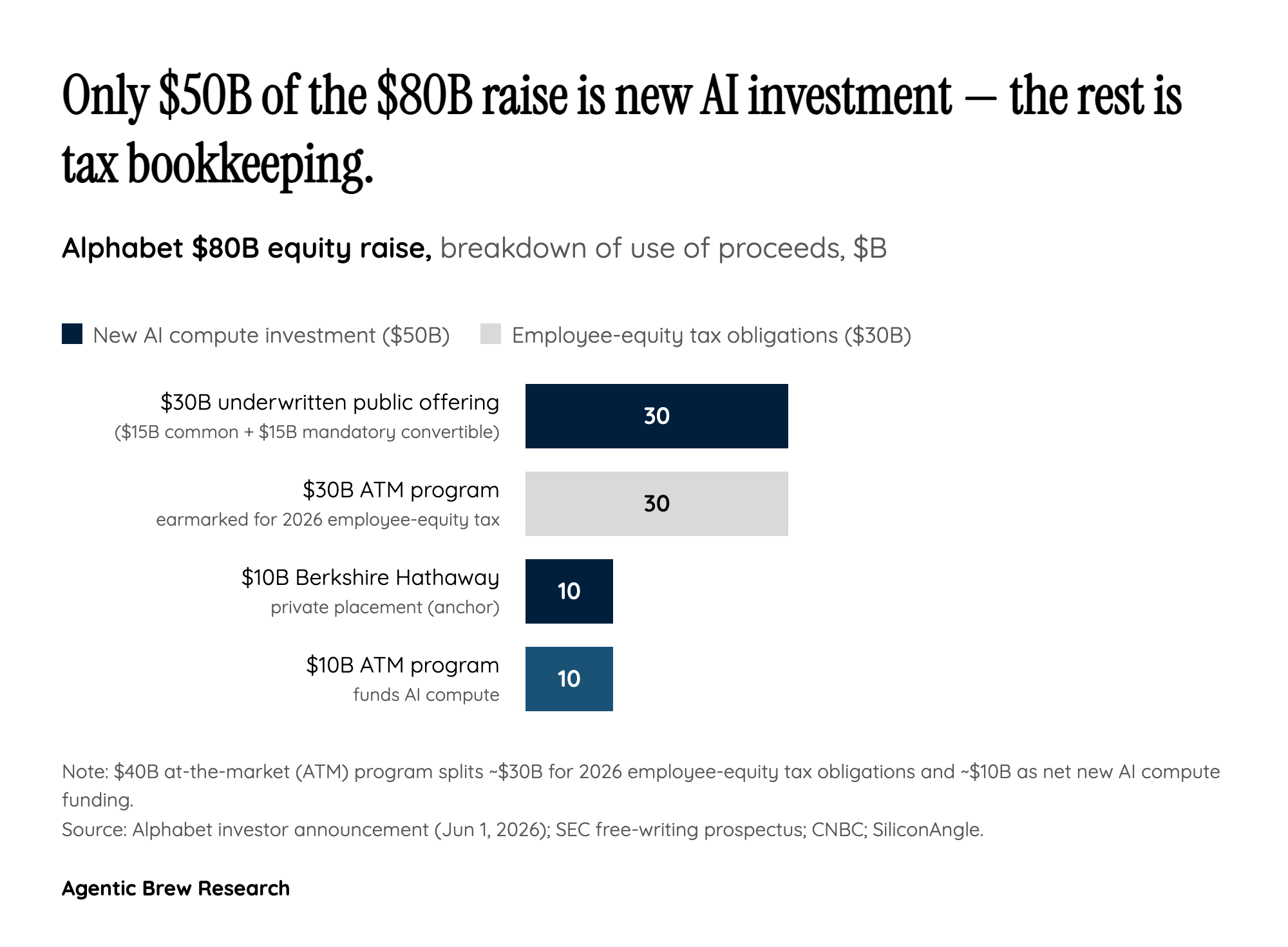

On June 1, 2026, Alphabet announced its first major stock offering in roughly twenty years [1]. CEO Sundar Pichai had spent the prior quarter publicly identifying compute capacity — not user demand, not model quality, not product-market fit — as his top operational worry, calling out 'power, land, supply chain constraints' as the gating factors on how fast the company can ramp AI services [2]. The raise is the financial expression of that worry. Google Cloud grew 63% year-over-year with a backlog of roughly $462B [2]— but Alphabet says demand at that level is 'exceeding the company's available supply.' Selling equity is what you do when your internal cash machine, however large, no longer keeps pace with the spend you have already committed to.

The shape of the deal underscores how unusual this moment is. Alphabet's free cash flow base — which CNBC notes is expected to mostly evaporate as capex doubles [9]— would not, on its own, fund the new spending plan, and Wall Street had been modeling continued buybacks instead. 2026 capex guidance jumped to $180-190B — roughly twice 2025's $91.4B spend [3]— and the CFO has flagged that 2027 will go 'significantly higher.' When the largest cash-generating ad business in tech cannot internally fund its own AI compute roadmap, that is the story. The market read it that way: GOOGL dropped about 2.27% on the announcement to $367.94 [4], while the broader hyperscaler complex traded on the implication, not the dilution. Community reaction across investor X and Reddit converged on the same point — the limiting factor for AI is no longer demand, models, or products, it is compute supply.