The Pop Was the Plan

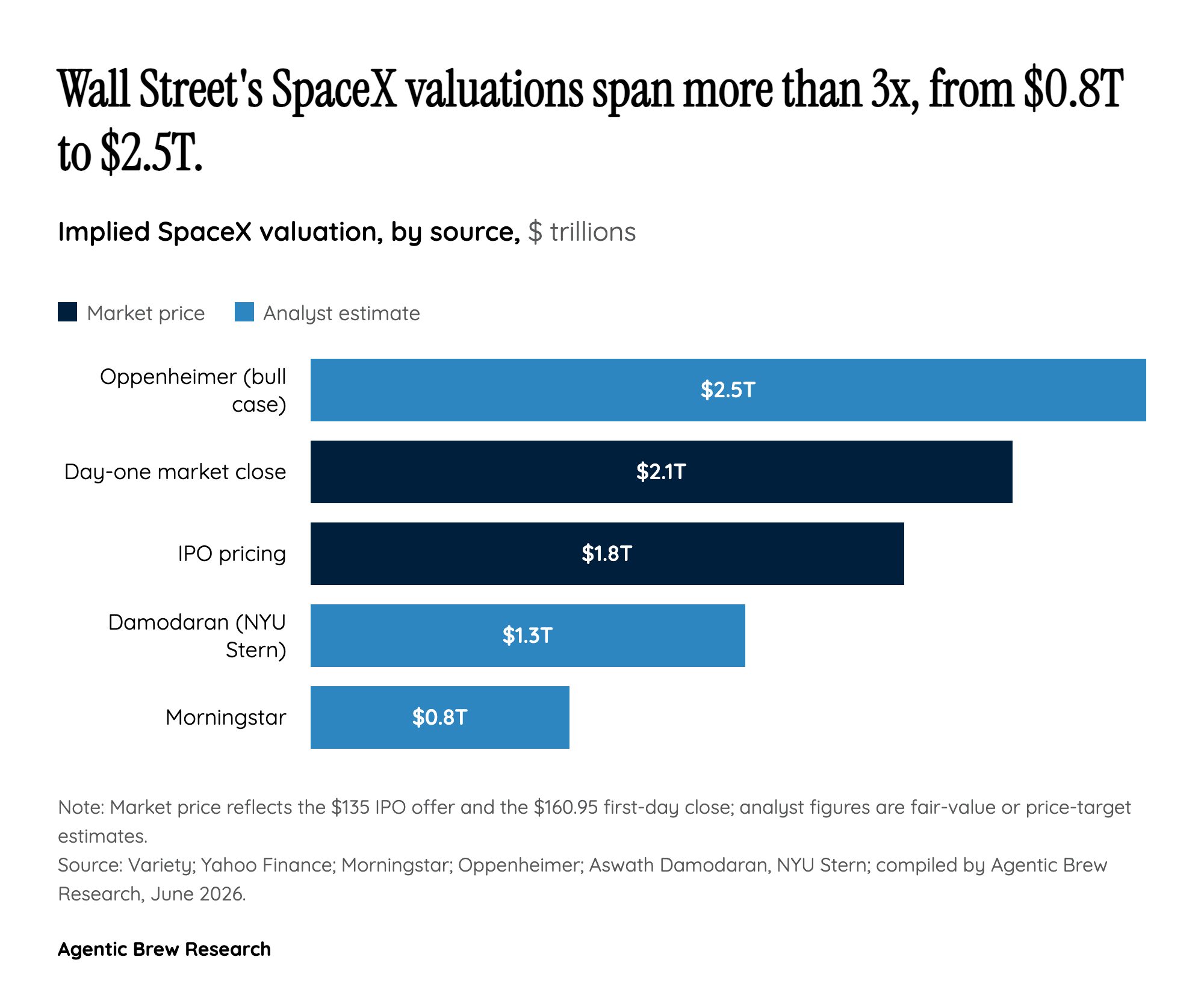

SpaceX did not so much discover a price as decree one. The shares were fixed at $135 before the roadshow even began, with no range and no book-building tug-of-war, making this the largest IPO in history at roughly $75 billion raised [4]. The stock then opened on the Nasdaq at $150, more than 10% above the offer, and closed its first day at $160.95, a 19.2% gain that lifted the company to a roughly $2.1 trillion market capitalization [1]. On a $75 billion raise, that one-day jump represents billions of dollars SpaceX could have captured for itself and instead handed to the investors lucky enough to receive an allocation. Yet the banks are unlikely to mourn it: SpaceX accepted a record-low 0.75% gross underwriting spread, and Fortune estimated the soft-dollar windfall flowing back to the syndicate, led by Goldman Sachs, which controlled the share allocation, could exceed $5 billion [2]. The discount was less a gift to the public than a lever the underwriters could pull to reward their best clients.

The more consequential machinery sits in the index plumbing. Nasdaq quietly revised its methodology effective May 1, 2026, so that a top-40 company by market cap can join the Nasdaq-100 after just 15 trading days, with no minimum-float requirement [3]. That rule turns the passive index funds that track the Nasdaq-100 into forced buyers of SPCX within weeks, regardless of price. The S&P 500 went the other way: after backlash, S&P Dow Jones Indices reversed a fast-track plan and kept its 12-month seasoning and profitability tests, which, given SpaceX's losses, block inclusion until at least mid-2027 [3]. The result is a stock with a thin public float, an unusually high retail allocation, and a guaranteed wave of mechanical demand bearing down on it.