The Commodity Maker That Out-Margined Nvidia

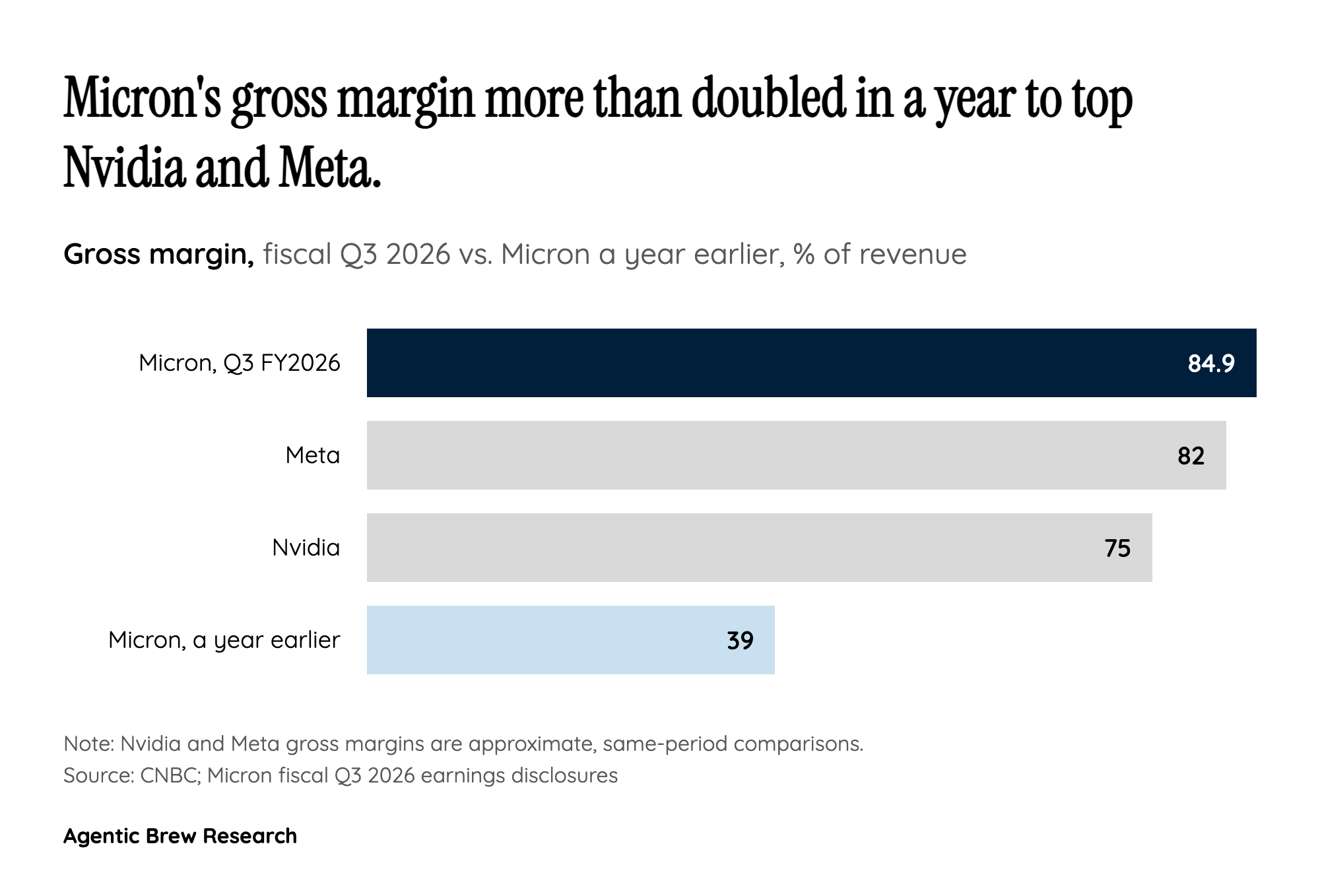

For most of its history Micron has been the textbook cyclical commodity business: it makes interchangeable memory chips, competes mainly on cost, and watches its margins collapse every time supply catches up with demand. Q3 2026 inverted that story. Micron's 84.9% gross margin did not just beat its own prior records, more than doubling from a year earlier, it surpassed Nvidia's roughly 75% and Meta's roughly 82%, the two companies most associated with AI value capture [1]. A memory maker is now keeping more of every revenue dollar than the company designing the accelerators and the company building the largest AI platform.

The mechanism is scarcity, not better silicon. High-bandwidth memory (HBM) stacks many DRAM dies vertically and sits next to a GPU to feed it data fast enough to keep its compute units busy. Because every modern AI accelerator needs a large allotment of HBM, and because HBM is far harder to manufacture than ordinary memory, the chip that used to be a passive component became the gating part of the entire AI stack. When the part everyone needs is sold out, the supplier sets the price. That is why Micron, historically the price-taker, briefly became the highest-margin name in big tech, reframing who actually captures the economics of the AI boom.