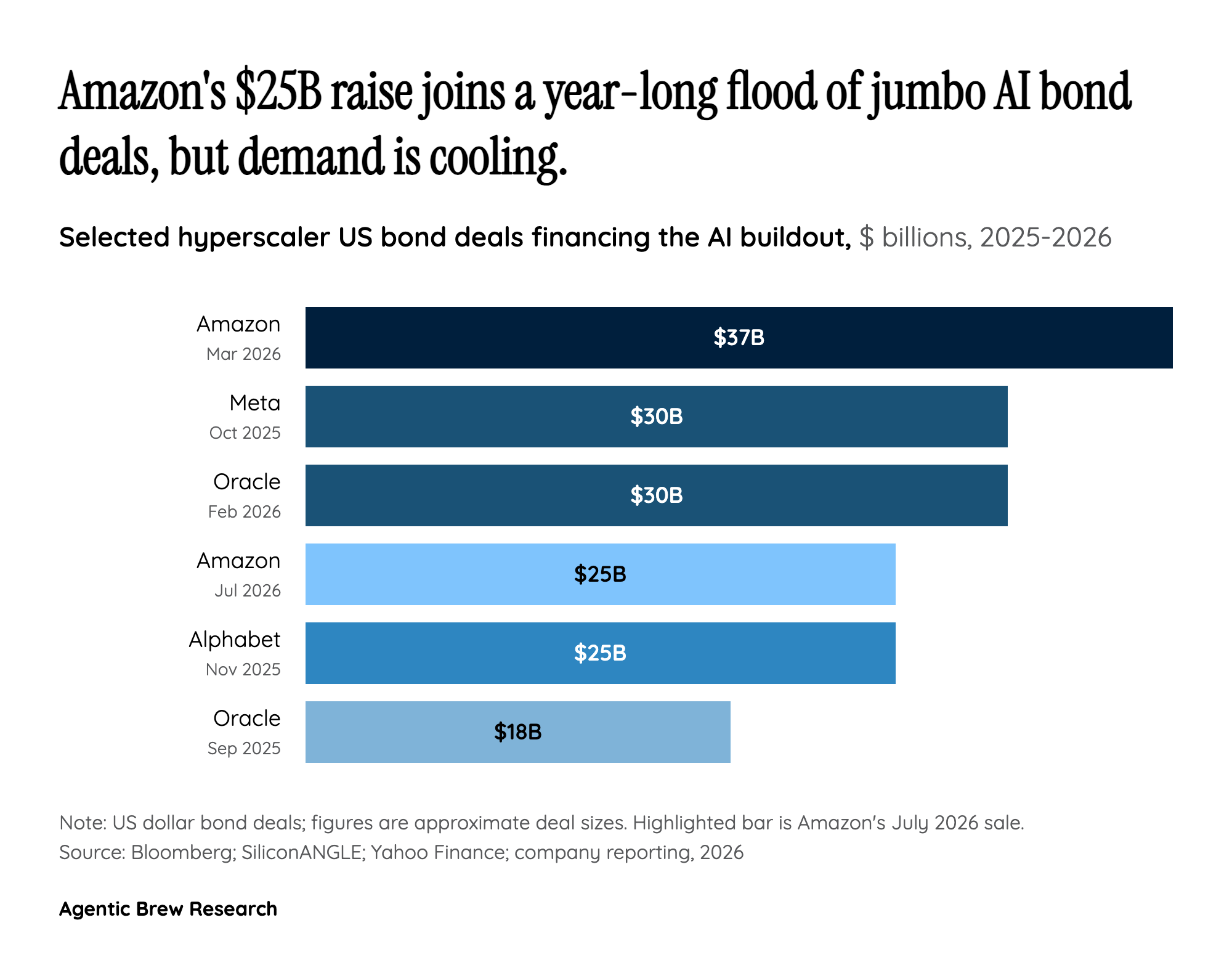

The Deal Sold - But the Enthusiasm Did Not

Amazon got its money. The story is what it cost to get it. When Amazon sold its biggest-ever bond earlier in 2026, it was inundated with orders on the back of AI-boom optimism. This time the reception was measurably cooler: peak demand for the eight-part offering reached roughly $62 billion, about half the orders the March deal drew, and the book ultimately pared back to around $41 billion [2]. That works out to roughly 1.6 times the deal size, well short of the roughly 4-times oversubscription that has been average for US high-grade sales in 2026 [1].

The gap matters because bond demand is a real-time referendum on how much AI debt investors are willing to keep buying. Amazon remains a top-rated, cash-generative borrower, so this is not a credit scare. It is an appetite problem. With this sale, Amazon's total bond issuance has climbed to more than $100 billion over the past year [2], and even a balance sheet that strong is starting to test how much paper the market will absorb without demanding a richer price.