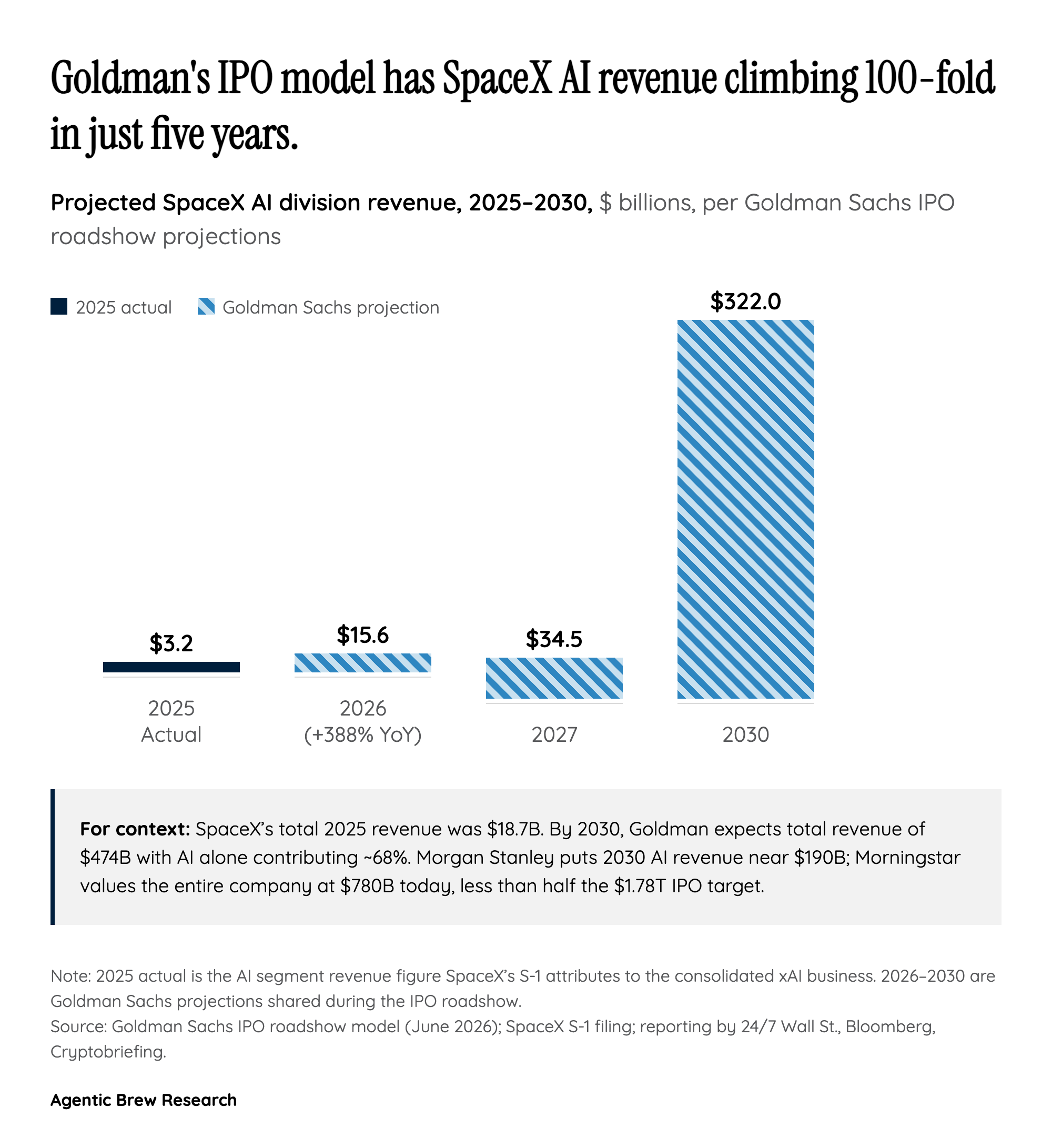

The 100x Forecast IS the Valuation

SpaceX did $18.7 billion in revenue in 2025 against a $4.94 billion net loss and a $41.3 billion accumulated deficit, with the consolidated xAI segment alone bleeding $6.36 billion [1]. None of those numbers support a $1.75 trillion market cap on any conventional multiple — the implied figure is 94 times trailing sales, and 107 times when adjusting for one-time items [2]. The only way to back into the valuation is to assume the AI division grows roughly 100-fold in five years.

That is exactly what Goldman Sachs's IPO roadshow model does. The bank projects AI revenue at $3.2B in 2025, $15.6B in 2026 (a 388% jump), $34.5B in 2027, and $322B in 2030 — total 2030 revenue of $474B with AI alone contributing about two-thirds of the company [3]. By 2031 the model has adjusted EBITDA at $352B (versus $6.6B in 2025) and free cash flow flipping from negative $13.8B to positive $72B [3]. Strip the 100x AI ramp out and the math collapses: the rocket and Starlink businesses, however good, do not justify a 7-week valuation jump from $800 billion to $1.78 trillion [4].

Goldman analysts have effectively published a single number — $322 billion of 2030 AI revenue — that has to be true for the IPO to be priced rationally. This is not a sensitivity case or one scenario among many. It is the load-bearing wall. Strip it out and the next-highest credible valuation is Morningstar's $780 billion fair value — Starlink at $611B plus roughly $170B of probability-weighted AI optionality — implying that buying at the IPO price is paying for a 100x AI scenario at near-certainty [8].