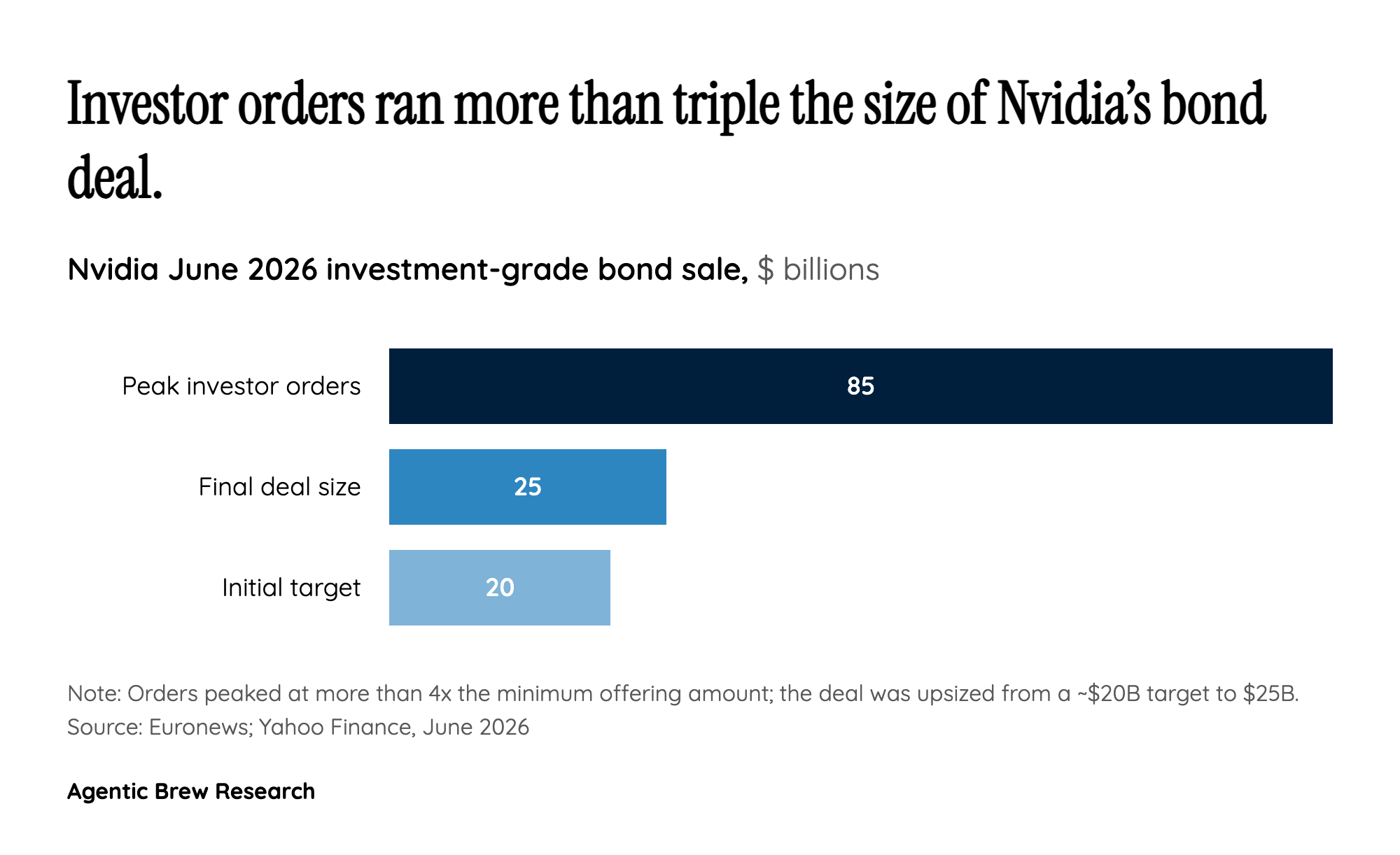

The cash-rich-company-borrows paradox

The puzzle that dominated community reaction is genuine: why does a company as cash-generative as Nvidia need to borrow $25 billion? The answer is that Nvidia's AI ambitions now outrun even its formidable cash generation, and debt lets it preserve cash while avoiding shareholder dilution [1]. Nvidia has been writing very large checks across the AI stack — $5 billion into Intel, up to $10 billion pledged to Anthropic, and $30 billion contributed to OpenAI's latest funding round [1]. Funding those commitments with equity would dilute shareholders; draining the cash pile would strip its strategic flexibility. Borrowing — especially at investment-grade rates — is simply the cheapest lever.

As Bloomberg Intelligence senior credit analyst Robert Schiffman framed it, inexpensive long-dated debt lowers Nvidia's weighted average cost of capital (the blended cost of financing itself through both debt and equity) and helps bankroll its AI investments without threatening its AA credit rating [1]. The Reddit r/StockMarket crowd reached the same conclusion organically: with a borrowing rate below inflation and AA credit at its strongest, locking in cheap money now reads as a rational move rather than a sign of distress.