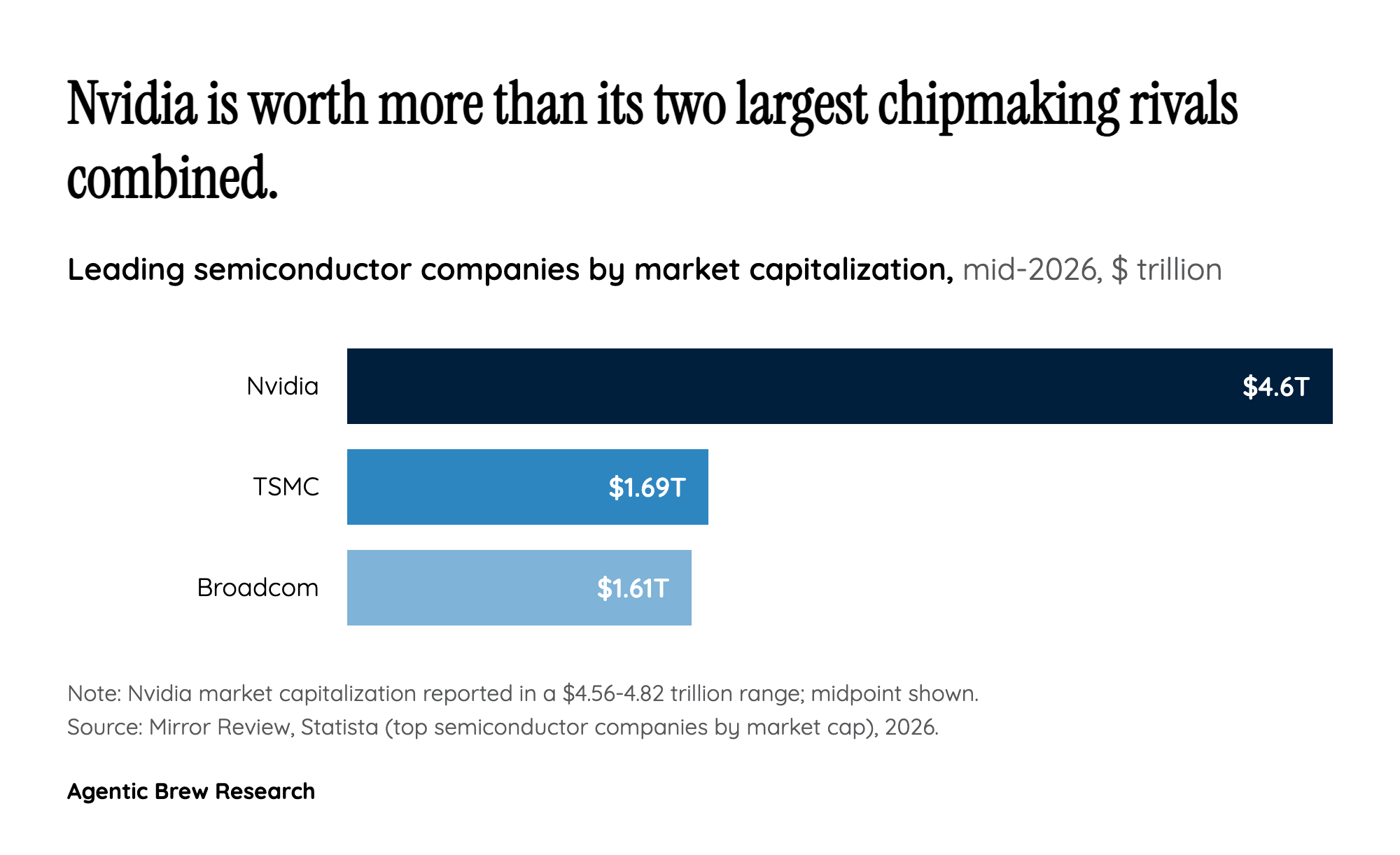

The week-before-IPO compute deal that markets can't agree on

Timing is everything here. SpaceX disclosed that Google would pay it $920 million per month from October 2026 through June 2029 for access to roughly 110,000 Nvidia GPUs plus CPUs, memory and related components, a contract estimated near $30 billion, just one week before SpaceX's stock was expected to start trading on Nasdaq [2]. The IPO itself is historic, targeting about $75 billion raised at a valuation around $1.75 trillion, with some intraday reads pushing past $2 trillion [2]. The bull read is straightforward: a marquee, multi-year, multi-billion-dollar revenue stream landing on the prospectus right before pricing. The skeptical read is harder to dismiss. Pointing to Google's standing as one of SpaceX's largest institutional investors, parts of the investing community framed this as circular financing, an investor effectively routing money back to inflate the asset it is about to take public. That same suspicion echoed at the top of the market: investor Michael Burry reportedly labeled the broader Nvidia-xAI chip arrangement "fugazi." The countervailing crowd waved him off, joking that he has predicted far more crashes than have ever arrived, and the community split cleanly between 2008-bubble analogies and traders dismissing the doom. What is not in dispute is the underlying hardware story: this capacity was originally built by Musk for xAI, which lagged competitors, so leasing it to Google and earlier to Anthropic turns a sunk cost into recurring revenue [5].