The math of the burn: spending built on credit, not cash flow

The defining financial fact of 2026 is that AI investment has decoupled from the cash that funds it. The four largest hyperscalers are set to spend $630 to $700 billion on infrastructure this year, roughly double 2025, pushing total industry outlays past $1 trillion [3]. That figure is no longer covered by operating profits: analysts cited in coverage of the cash crunch warn big-tech free cash flow could fall as much as 90 percent in 2026 as capex outpaces AI revenue [1]. Venture capital shows the same concentration, with AI capturing roughly 80 percent of all global venture funding in Q1 2026 [7].

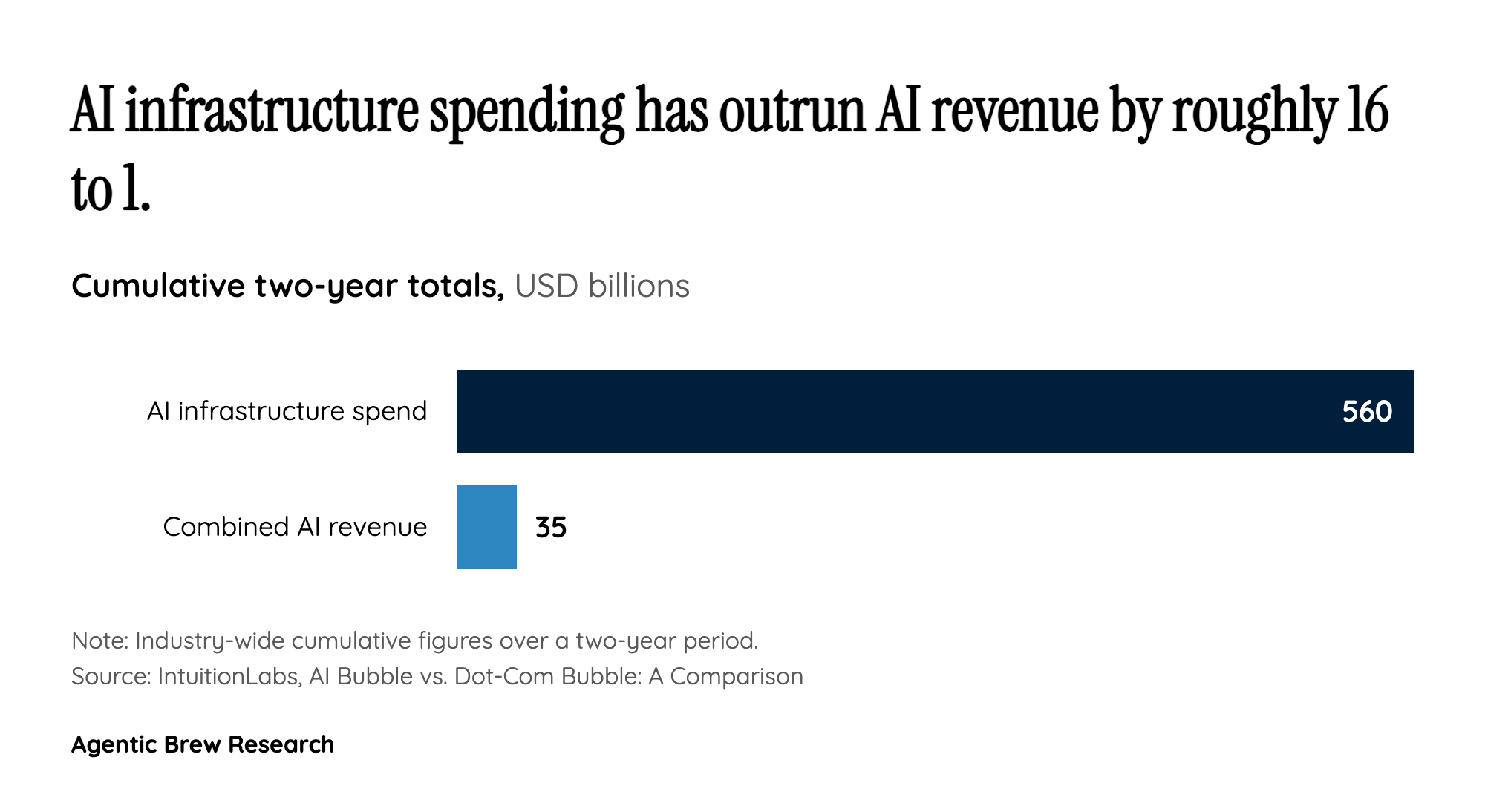

The gap between spend and income is being bridged with credit. As capex outstrips free cash flow, the buildout is increasingly debt-financed, much of it through off-balance-sheet vehicles and undisclosed lease commitments that obscure how much leverage is actually in the system [2]. The capex-to-sales ratio is projected to hit 34 percent in 2026 and 37 percent by 2028, exceeding even the dot-com era's 32 percent, with cumulative AI spending of roughly $2 trillion expected across 2026 to 2028 [2]. At the company level, OpenAI is the sharpest illustration: $3.7 billion burned in Q1 2026 against $5.7 billion in revenue, roughly $14 billion in annual burn, and a $50 billion compute plan funded out of a $73 billion cash pile [8]. Even the largest balance sheets are now reaching for layoffs, stock sales, debt issuance, and public offerings to keep the buildout funded [1]. The historical scale gap is stark: roughly $560 billion went into AI infrastructure over two years against about $35 billion in combined AI revenue [9].