The dilution math that spooked the market

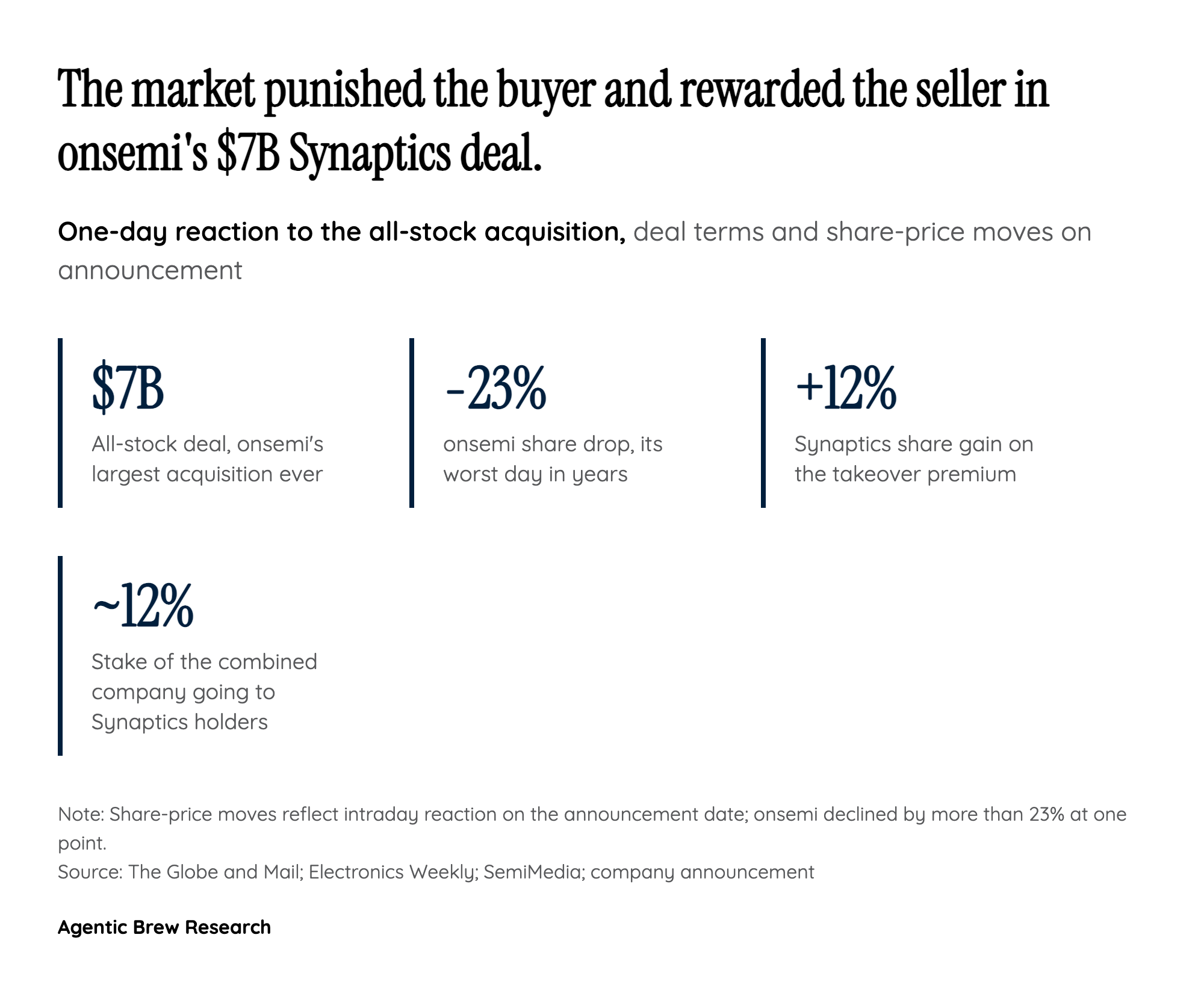

The structure of the deal, not just its size, is what triggered the sell-off. onsemi is paying roughly $7 billion entirely in stock, exchanging 1.350 onsemi shares for each Synaptics share at about a 19 percent premium to the target's 10-day VWAP [1]. Because no cash changes hands, the cost is borne directly by existing shareholders through dilution: Synaptics holders are expected to own about 12 percent of the combined company on a fully diluted basis [1]. That handover of equity, layered on top of an already transformational change to onsemi's business, was a key driver of the crash [4].

The market's verdict was swift and severe. onsemi shares fell roughly 20 to 23 percent on the announcement, declining by more than 23 percent at one point during the session and marking one of the company's worst days in years [4][5]. The mirror image played out at Synaptics, whose shares rose about 12 percent as investors priced in the takeover premium [3]. The split reaction is the cleanest signal of where the perceived value transfer landed: toward the acquired, away from the acquirer.