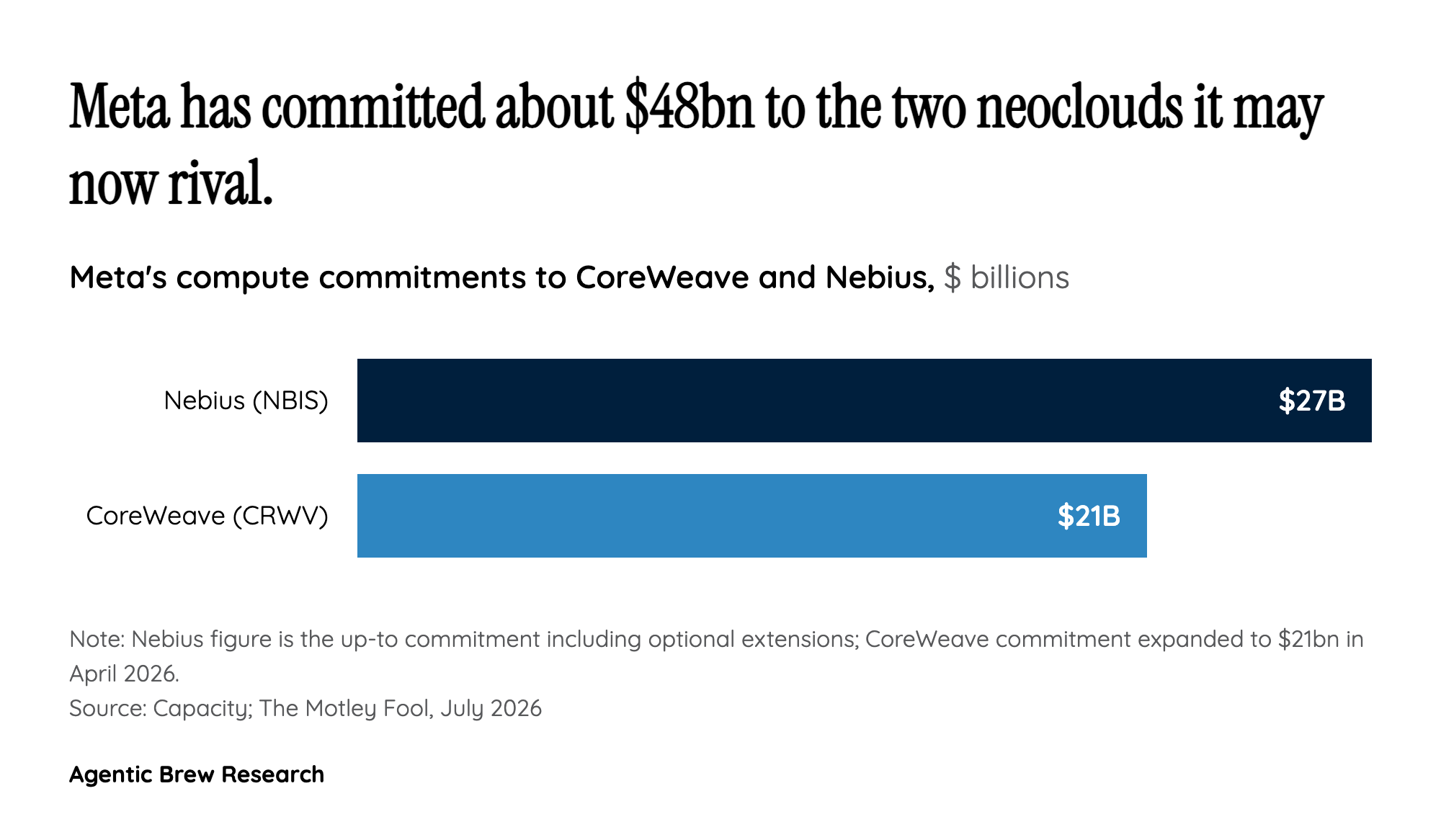

Two tracks, one threat: only the raw GPU rental competes with neoclouds

The name to internalize is Meta Compute, and it is really two businesses wearing one label. The first track sells hosted access to Meta's own models - including its Muse Spark models - on Meta's infrastructure, an approach explicitly compared to AWS Bedrock [1]. The second track sells raw computing capacity, the bare rental product that specialist neocloud providers rent out today [4]. Only that second track puts Meta head-to-head with CoreWeave and Nebius; the Bedrock-style track competes more with model-hosting layers than with GPU landlords. That distinction matters because the market sold both neoclouds as if Meta had announced a pure rental war, when the reported plan is a portfolio in which raw rental is one option among several. SemiAnalysis maps four distinct use cases behind the fleet - frontier model training in Superintelligence Labs, scaling ad recommendation systems more than tenfold in complexity, hosting private Claude instances via Anthropic, and selling high-margin compute - none of which resemble a commodity rental business [2].