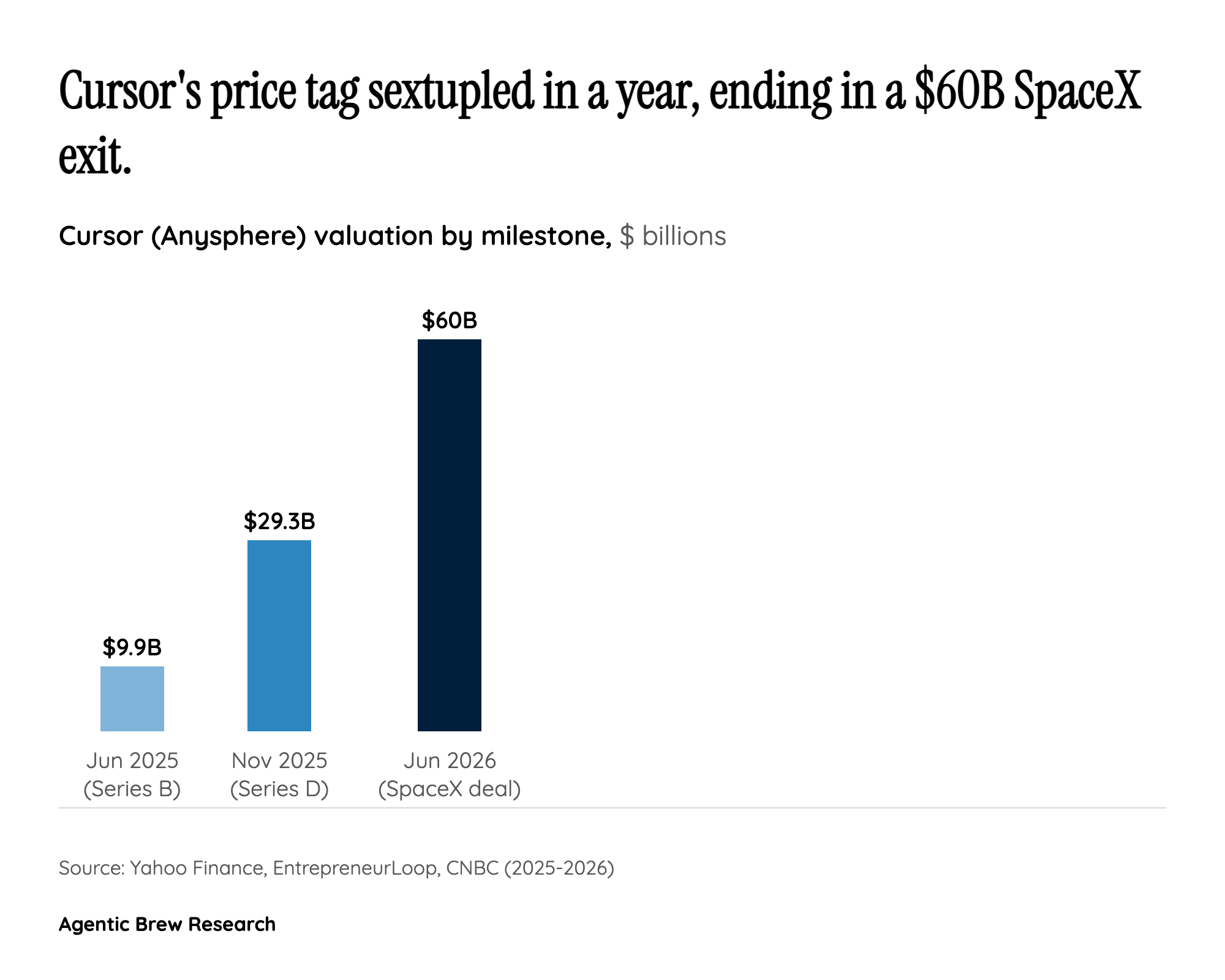

Paying $60 Billion With Money That Didn't Exist Last Week

The most striking feature of this deal is that almost none of it is cash. SpaceX is buying Cursor entirely with its own freshly-minted Class A stock, days after a Nasdaq debut that floated only about 4% of its shares [1]. That tiny float is the whole trick: when a company sells only a sliver of itself, scarcity alone can push the price up, and SpaceX's stock jumped roughly 50% from its $135 offering price, briefly carrying the company past a $2.9 trillion valuation and ahead of Amazon [2]. A richly-valued share is now a currency, and the company is spending it.

The deal's structure quietly compounds this. The exchange ratio — how many SpaceX shares each Cursor owner receives — is set by the volume-weighted average of SpaceX's closing price over the seven trading days before the deal closes [3]. In plain terms: the higher SpaceX's stock trades into closing, the fewer shares it has to print to cover the same $60 billion. The incentive to keep the stock elevated through Q3 is baked into the contract.

What makes this remarkable is the contrast with the underlying business. SpaceX lost $4.9 billion on $18.7 billion of revenue in 2025, with Starlink the only consistently profitable part, and the Guardian notes the purchase does not draw on the IPO proceeds at all [4]. A company burning billions a year is acquiring a $60 billion company without spending a dollar of operating cash. The reaction split along exactly this fault line: euphoria on X greeted the deal as the largest software acquisition in history, while Reddit's finance and technology communities were openly cynical, framing it as creating paper value out of thin air to buy real companies and reaching for Cisco-era dot-com comparisons.