Why a cash-rich company borrows: the $20 billion puzzle

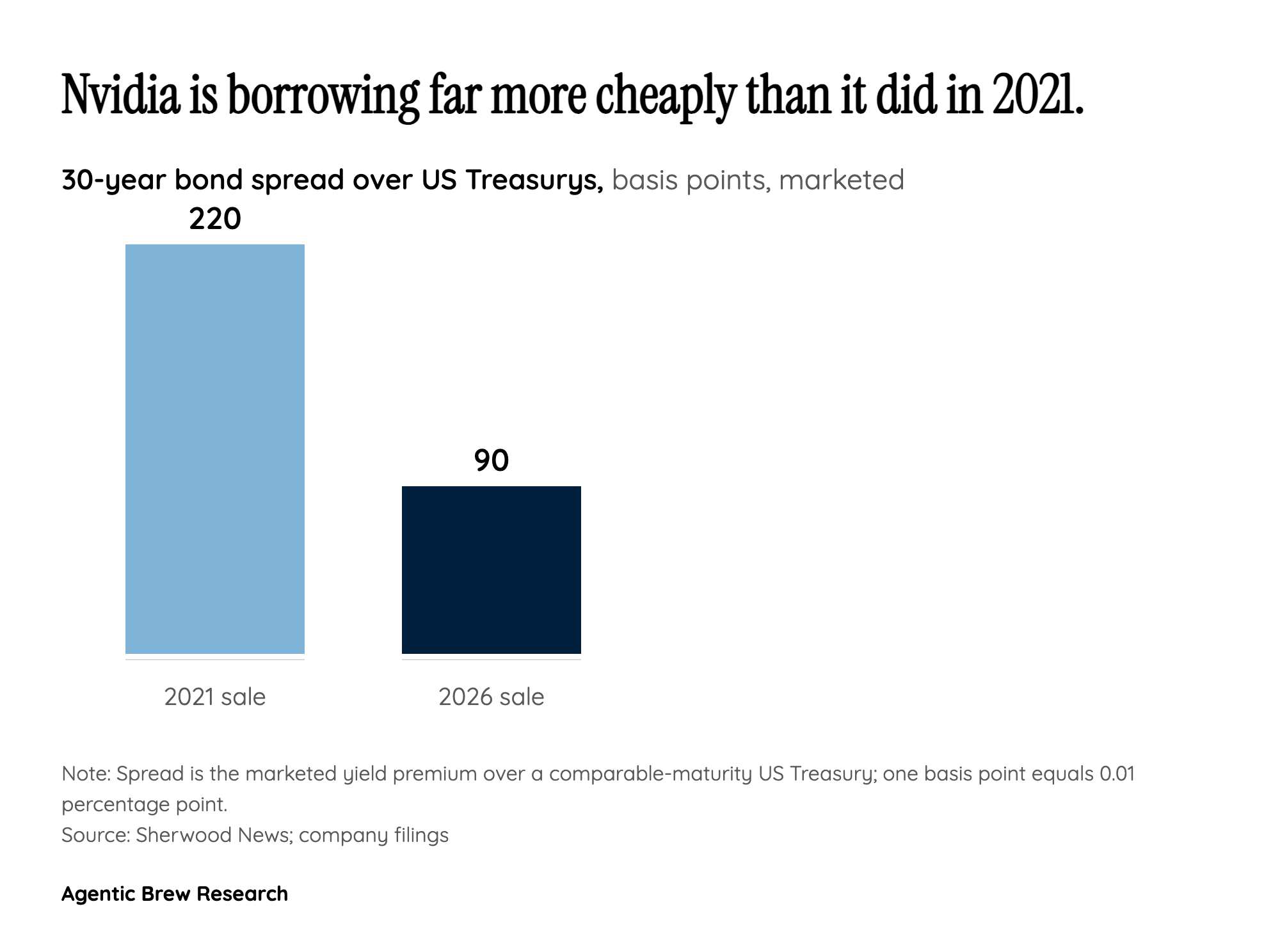

The first reaction to Nvidia tapping the bond market is bewilderment. This is the most valuable company on earth, a business that throws off enough cash to fund aggressive buybacks, and yet it is asking institutional investors to lend it at least $20 billion across seven tranches stretching out to 2056 [1]. Why would such a company borrow at all? The answer, as commentators have framed it, is less about need and more about price. With long-dated money available at under one percentage point above US Treasurys, the issuance reads as a balance-sheet optimization rather than a signal of distress [3]. As one markets columnist put it, 'when you can raise money through the mid-2050s at less than a percentage point above US Treasurys, I suppose you don't say no' [2].

There is a second, more strategic logic that runs underneath the opportunism. Debt is structurally cheaper than dilution: issuing new equity hands away ownership and future upside, while a bond simply costs interest. When that interest rate is competitive with inflation, the borrowing is close to free in real terms, and the proceeds free up the company's own cash for buybacks, research and development, and partnerships. The online debate around the raise circled exactly this point, with some observers noting that borrowing below the rate of inflation is precisely what a company does when it expects its stock to keep rising and would rather not sell shares to fund itself. CNBC's Jim Cramer raised the natural follow-on question, asking whether Nvidia, like Apple before it, might funnel the proceeds toward buying back its own stock, an implicit bet that its shares are undervalued [5].