Two Doors Into the Cloud: Bedrock's Twin, or CoreWeave's Understudy

Meta Compute is not one product but a fork in the road. The first path is a hosted AI model service modeled on Amazon Bedrock [1], where enterprises tap models - including Meta's own closed-weight Muse Spark and Llama - through APIs without managing infrastructure. The second is raw GPU compute rented as infrastructure-as-a-service, competing head-on with the neoclouds CoreWeave and Nebius [1].

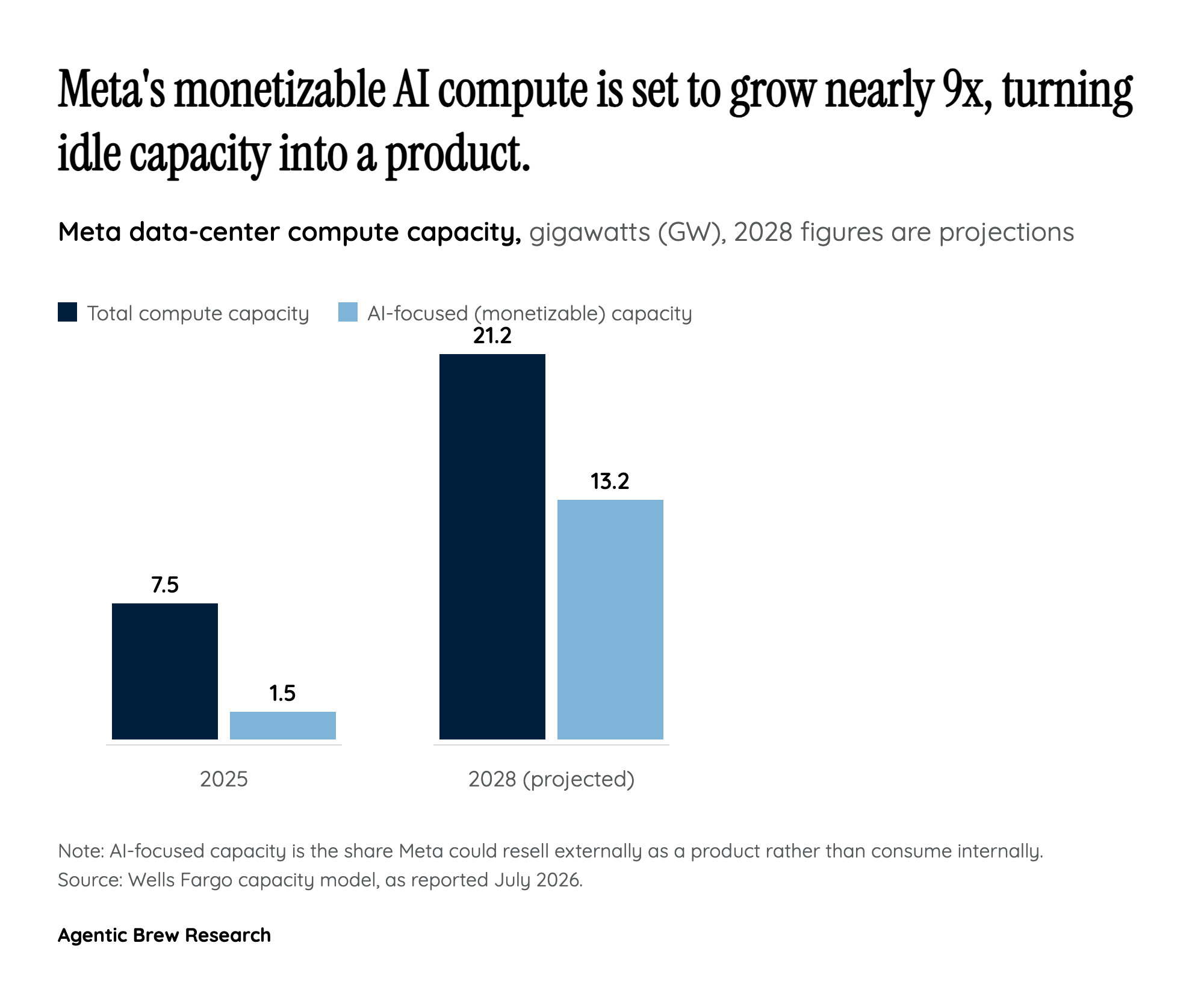

The two doors imply very different businesses. The hosted-model route keeps Meta higher up the value chain, bundling its software and models where margins can hold. The raw-compute route is closer to a commodity: renting out idle Nvidia capacity by the hour. That distinction matters because it decides whether Meta is selling something differentiated or simply becoming a landlord for GPUs. SemiAnalysis has framed the range of uses even more broadly - Meta could deploy this compute for its own models, ad scaling, SpaceX-style neocloud deals, or hosting third-party models, and may be close to an Anthropic hosting arrangement [6].