Renting out your own GPUs is either capex discipline or a confession

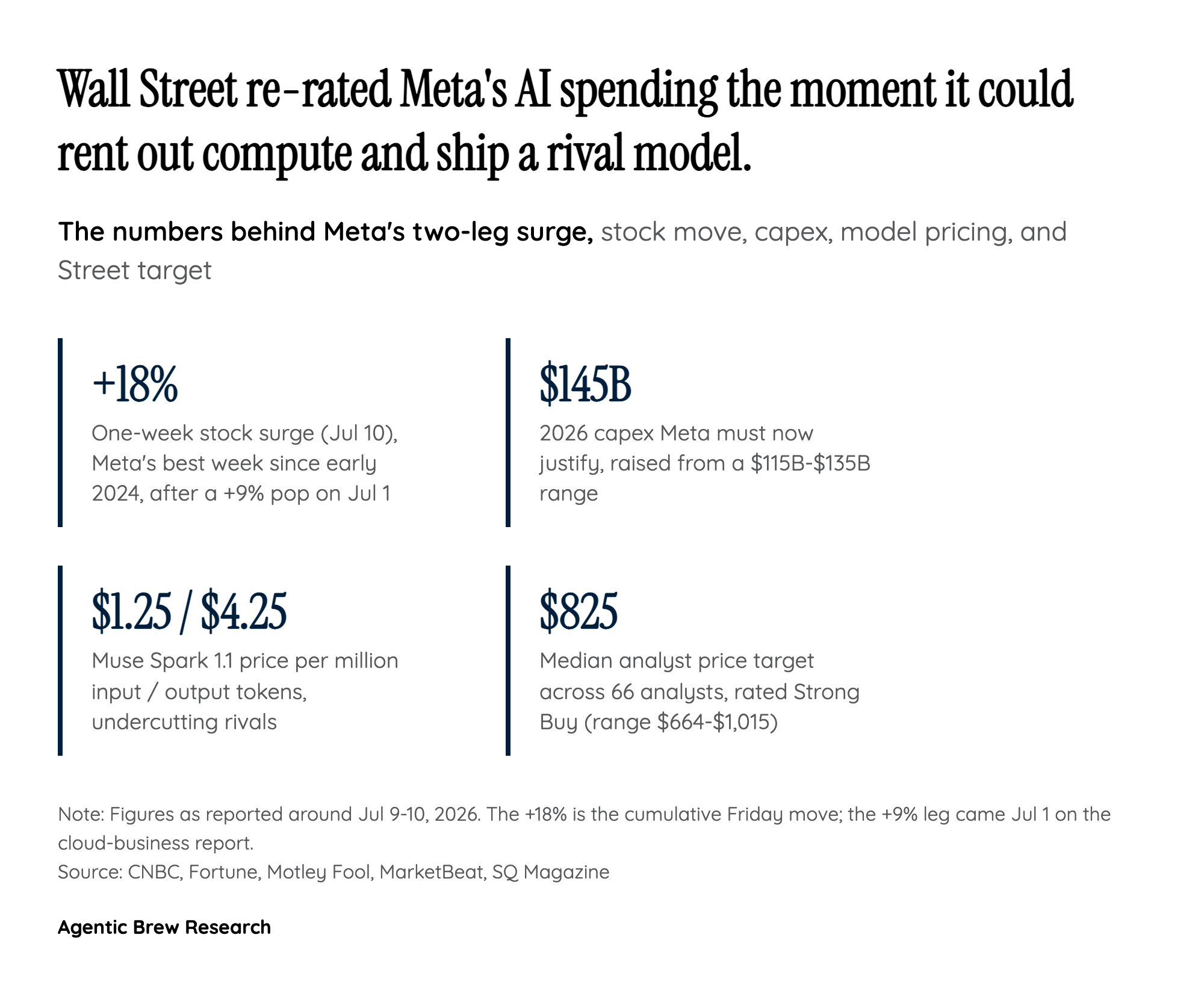

The market's core read on 'Meta Compute' is that Meta will lease surplus computing power to enterprise customers rather than let expensive data centers idle [1]. Bulls frame this as discipline: with Meta guiding 2026 capex to as much as $145B, raised from a prior $115B-$135B range and aimed largely at AI data centers, a compute-rental revenue path helps justify the spend and re-rate previously discounted infrastructure value [2][3]. The bearish counter-read, surfaced in community discussion, is that a company selling its 'excess' AI capacity is quietly admitting its own AI products cannot fill it. Both interpretations coexist in the tape, and that ambiguity is exactly why analysts must now weigh a lower-margin future against a fully-utilized-fleet upside.