The Collapse Is Only Half the Story - Who's Cutting and Who's Quietly Raising

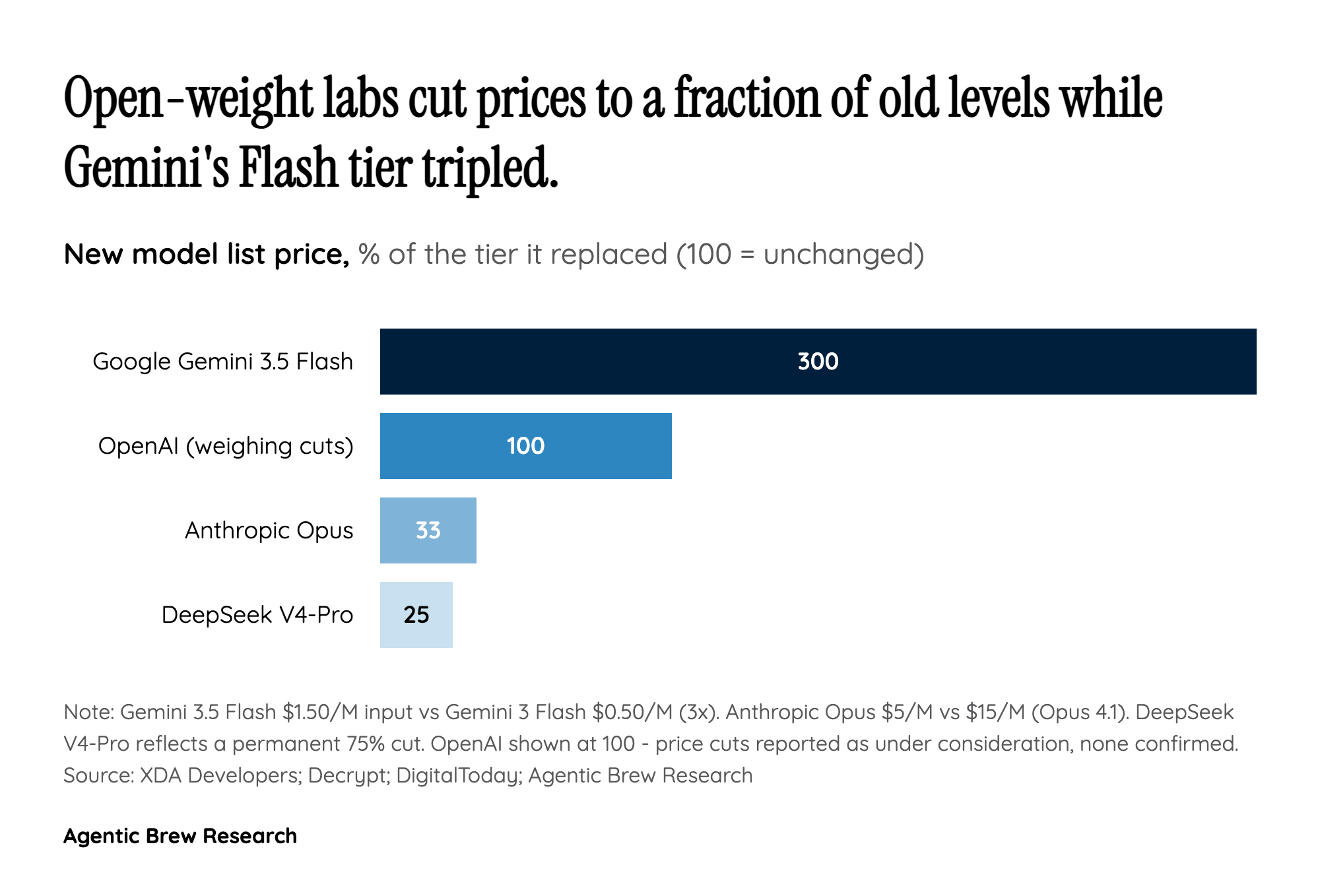

The headline that AI model prices are collapsing is true for one side of the market and false for the other. On the cutting side, DeepSeek made a 75% price reduction to its flagship V4-Pro permanent, landing it near $0.44 per million input tokens and $0.87 output - numbers that undercut GPT-5, Opus 4.7, and Gemini Flash by a wide margin [1]. Anthropic followed the gravity, dropping Opus from $15 per million to $5 per million, a roughly 67% cut [2]. OpenAI, per Wall Street Journal reporting, is weighing steep cuts of its own ahead of a confidential IPO filing [3].

But the model everyone was waiting on moved the opposite way. Google's Gemini 3.5 Flash launched at $1.50 per million input and $9 per million output - roughly a 3x increase over the Gemini 3 Flash tier it replaced [1]. One report frames this as the era of subsidized Western AI pricing coming to an end, arguing those low prices were never sustainable [1]. So the accurate picture is a two-sided market: open-weight labs are collapsing the floor while frontier tiers quietly lift the ceiling. Calling it a uniform collapse misses the actual competitive geometry - the cheap tokens and the expensive tokens are moving apart at the same time.