The Cleanest Read on AI Demand Yet, and the Market Shrugged

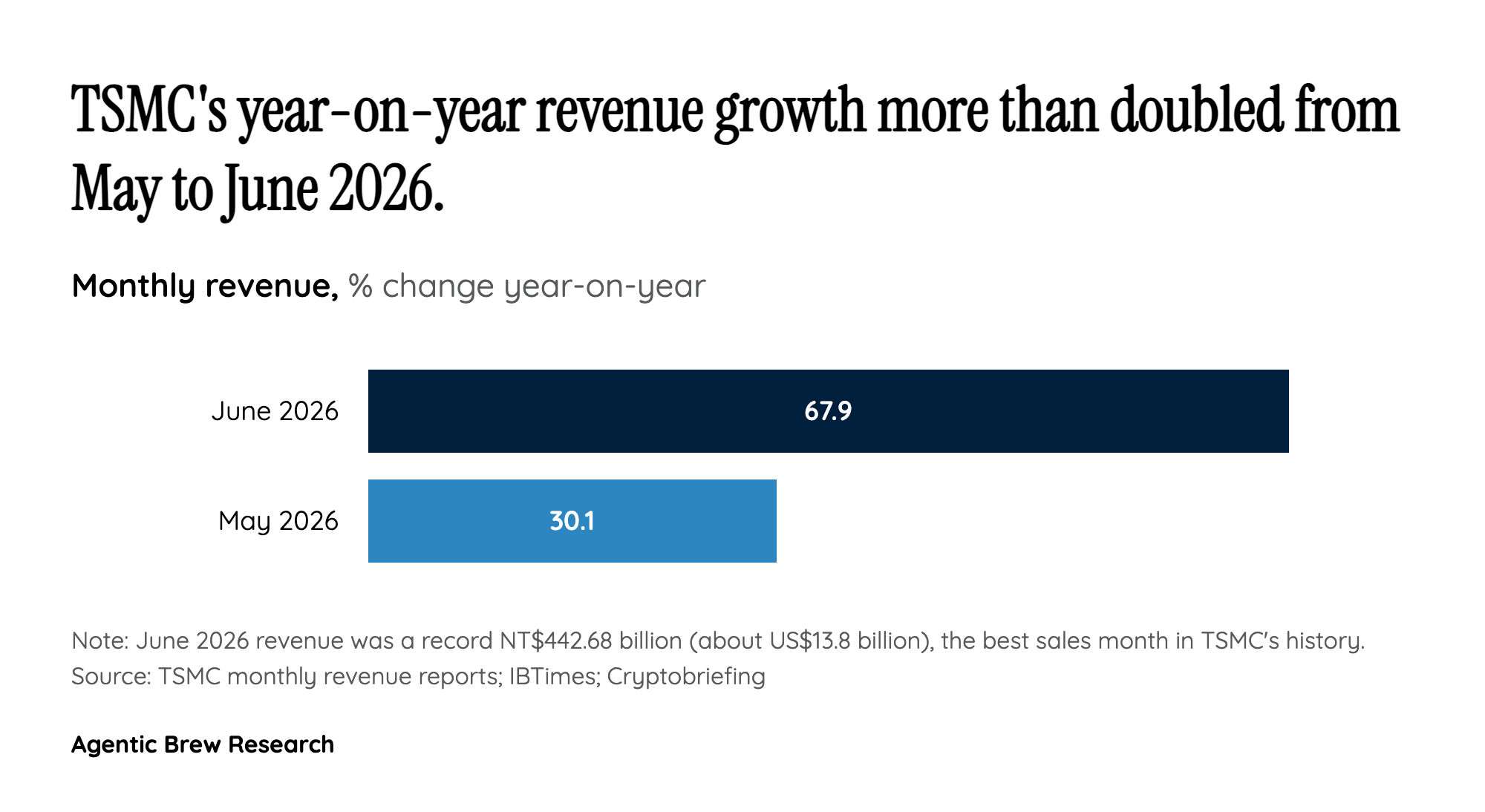

TSMC's June print is the single least ambiguous signal in the AI hardware cycle right now. At NT$442.68 billion it is the best sales month in company history, up 67.9% year-on-year and 6.2% above May [1]. Stacked up, the quarter reached roughly NT$1.27 trillion (~$39.6 billion), a 36% annual gain that cleared the top of TSMC's own $39 billion to $40.2 billion guidance [2]. Because TSMC fabricates the advanced silicon that nearly every AI accelerator depends on, its revenue functions as a demand meter that is harder to spin than any single customer's forecast. Yet the reaction exposed a tension: shares rose only about 1% on the update [3], and community reaction across investor forums centered less on the number itself, which was treated as unambiguously strong, and more on confusion that the stock did not fly. The prevailing read is that TSMC is now priced to perfection, where a record is merely the expected outcome and the risk has migrated from whether demand shows up to whether it can keep beating an already euphoric bar.