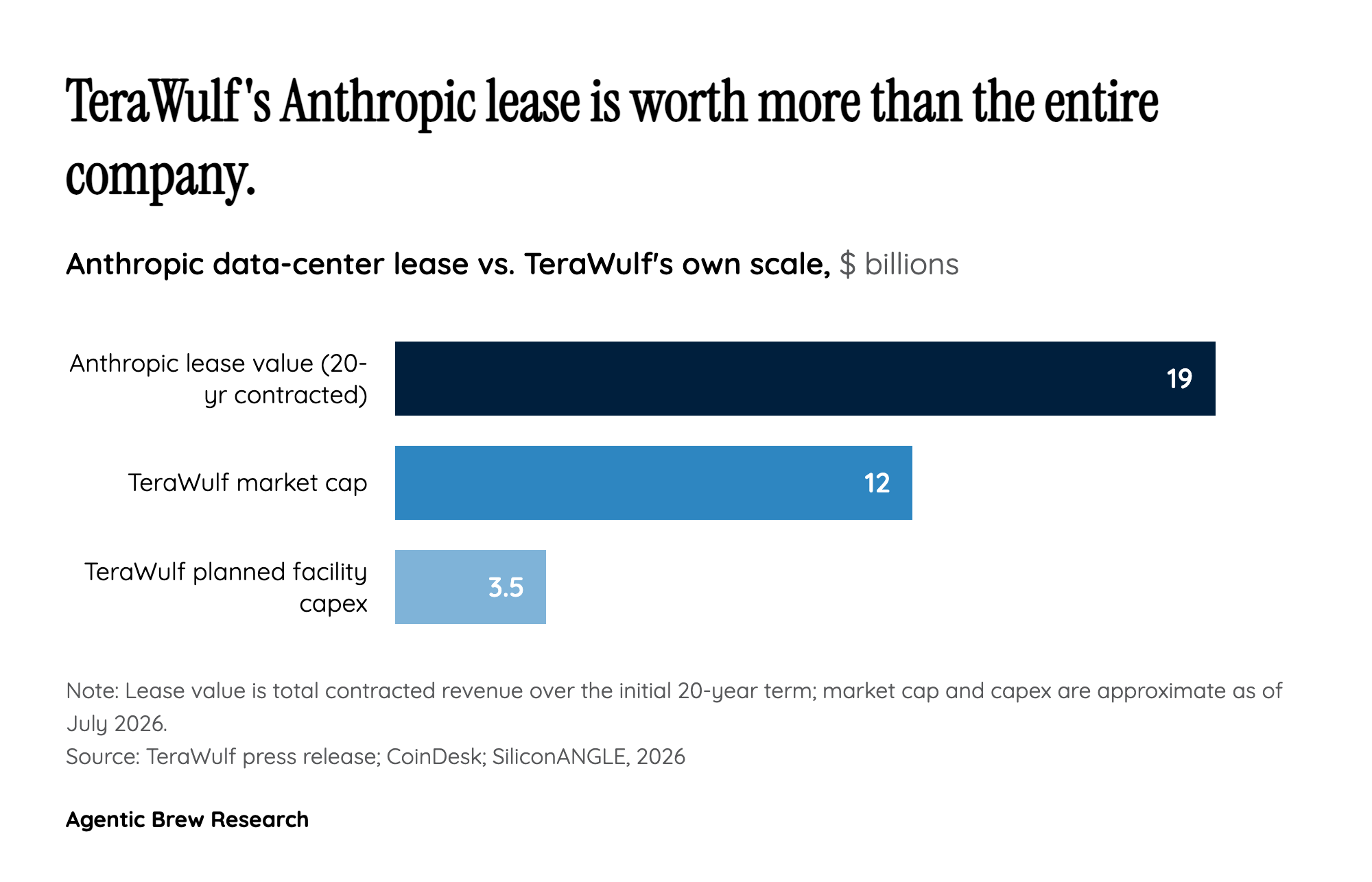

A $19 Billion Bet on Buildings That Don't Exist Yet

The headline number is staggering for a company TeraWulf's size: a 20-year lease expected to generate roughly $19 billion in contracted revenue, more than the miner's entire market capitalization of around $12 billion at the time of the announcement [1]. The campus that will house it does not yet exist - initial power is not expected until the second half of 2027, with the full 401 MW online by early 2028. Broken down, the lease implies about $950 million in annual revenue, or roughly $2.37 million per megawatt per year [2], a premium rate that reflects how much a frontier lab will pay to guarantee power years in advance.

The economics look even more lopsided from TeraWulf's side of the ledger. The company plans to invest only around $3 to $4 billion to build out the facility - less than a fifth of the lease's headline value - against last-quarter revenue of roughly $34 million [3]. In other words, a single tenant has just committed to pay TeraWulf, over two decades, a sum that dwarfs everything the company is today. That asymmetry is exactly why the stock reacted the way it did, and why the deal is being read as a template for an entire class of power-rich, cash-poor infrastructure owners.