The wafer war consumers were never told they joined

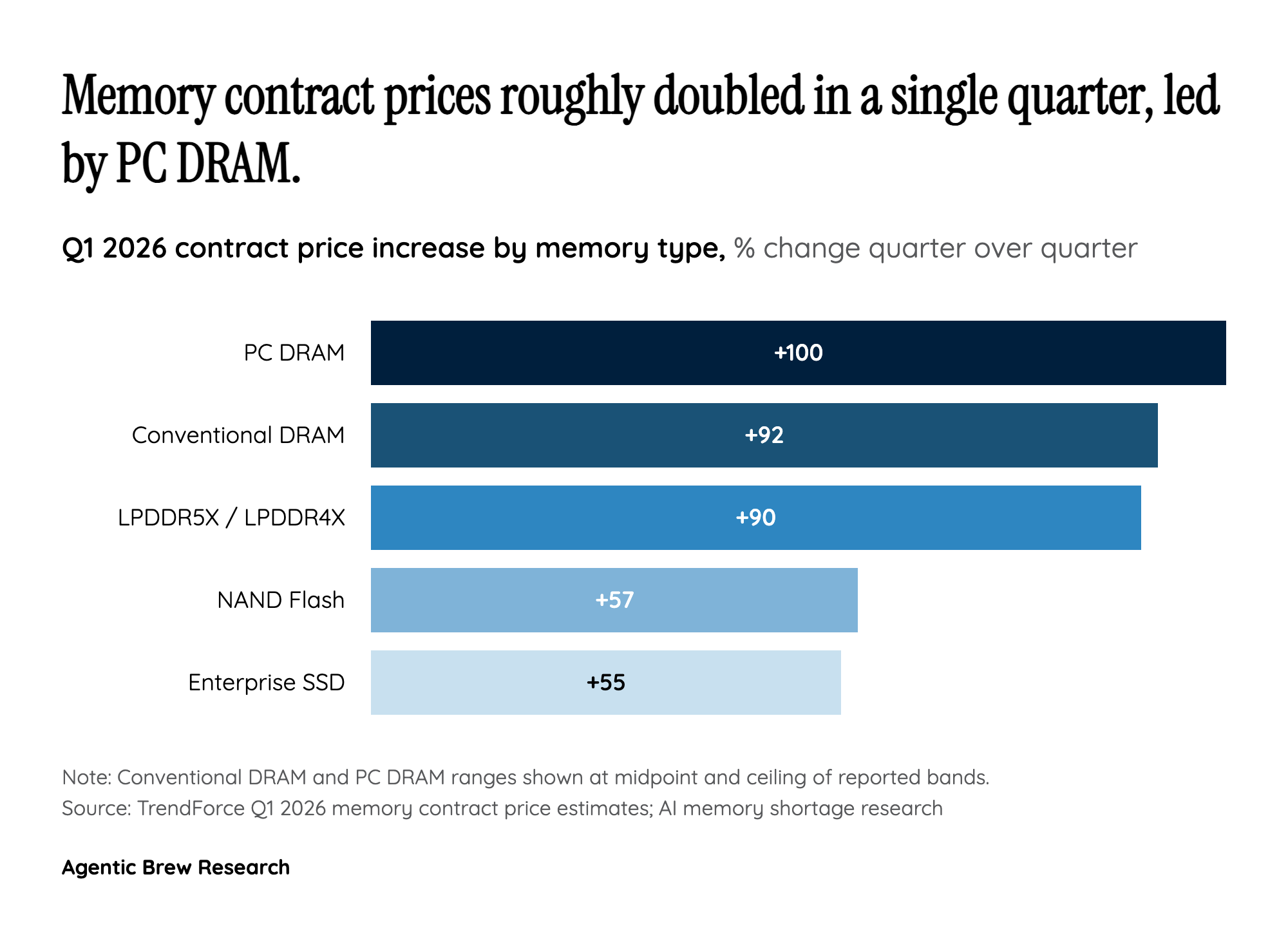

For two decades, memory was the part of your laptop you never had to think about - cheap, abundant, and deflationary by default. That assumption broke this year, and the break is structural rather than cyclical. DRAM prices rose roughly 172% across 2025 as channel inventory collapsed from twelve weeks to as little as two [9]. The three companies that control over 95% of global DRAM - Samsung, SK Hynix and Micron - have quietly redirected as much as 93% of their combined output toward high-bandwidth memory, the stacked DRAM that feeds AI accelerators [8][10]. IDC describes the shift bluntly as a potentially permanent, strategic reallocation rather than a temporary mismatch of supply and demand [6].

The economics behind that choice are unforgiving for anyone buying a phone or a PC. HBM commands margins three to five times those of conventional DRAM, and producing a single bit of it consumes roughly 300% more wafer capacity than DDR5 [7][10]. In other words, every wafer a maker pours into an HBM stack for an Nvidia GPU is a wafer it does not turn into the LPDDR5X module of a mid-range smartphone [6]. Data centers now absorb an estimated 70% of all memory chips produced worldwide, and HBM alone is set to take 23% of total DRAM wafer output in 2026, up from 19% in 2025 [6][8]. This is the mechanism that turned an AI capital-expenditure boom into a line item on consumer receipts.