The Cycle Everyone Thought Was Permanent Just Got Re-Priced

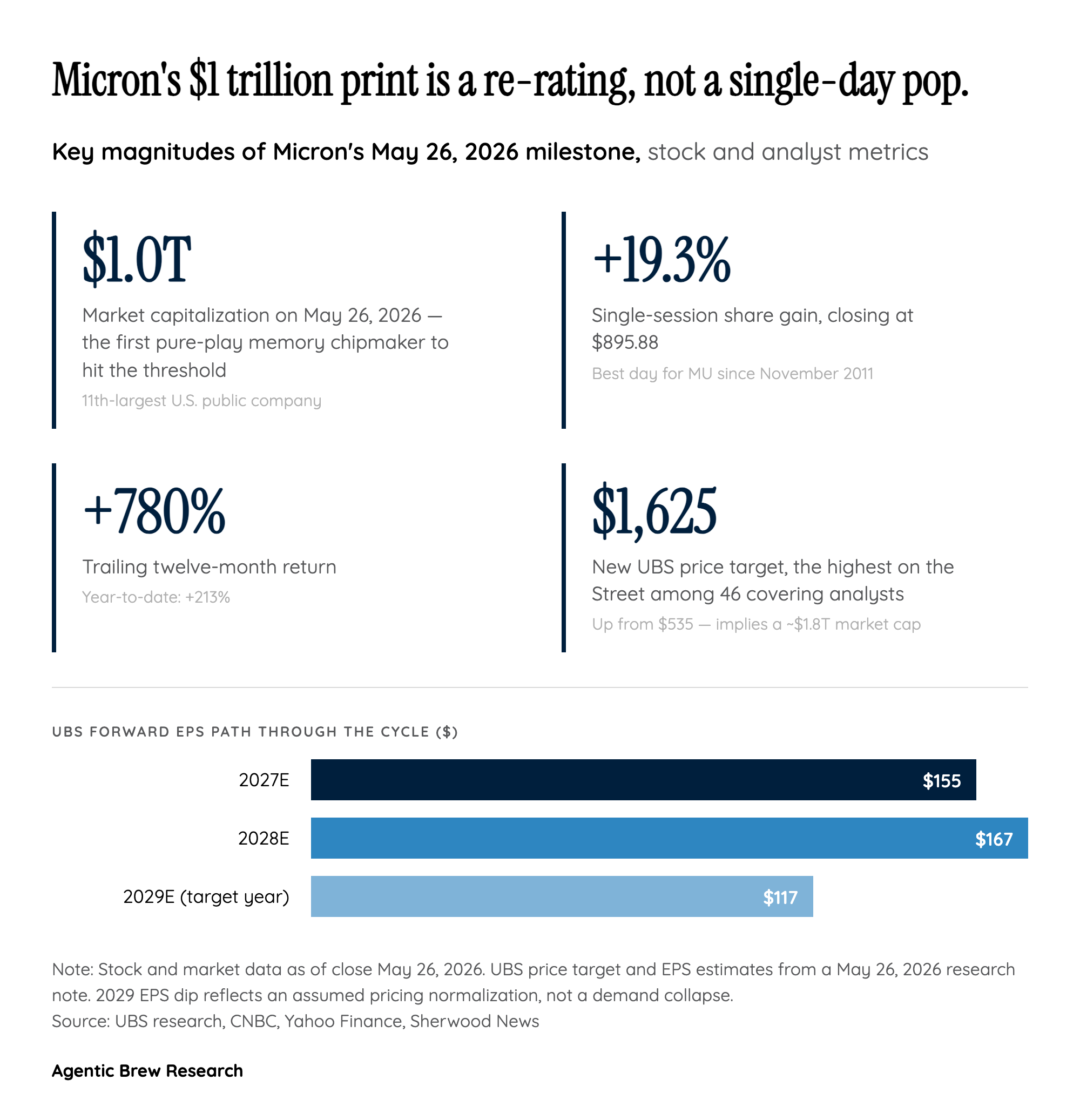

For four decades, the rule on memory was simple: it is a commodity, and commodity producers are valued on the next downturn, not the next quarter. DRAM glut cycles bankrupted competitors and held Micron's multiple at a fraction of its logic-chip peers. That assumption is what UBS's Timothy Arcuri just torched. Arcuri's new framework argues that the locked-in long-term agreements Micron has signed with hyperscalers — covering pricing and volume through 2029 — are functionally an infrastructure franchise, not a spot market. His direct words: 'We believe the market will start to put a more "normal" multiple on the stock and MU will continue to re-rate higher as more details emerge about the structural changes AI has driven to the entire memory complex' [1].

The Street is starting to agree. D.A. Davidson's Gil Luria put it bluntly — 'Memory companies are becoming less cyclical' [2]— and the price action ratified the view. Micron closed up 19.29% at $895.88, its best session since November 2011, on the way to the 11th-largest market cap among U.S. public companies [3]. Twelve months earlier, the same stock traded under $100.

What is being re-rated is not Micron's manufacturing. It is the predictability of its cash flows. If the contracts hold, a memory company starts to look like a utility with optionality. If they don't, the cycle takes back what it gave.