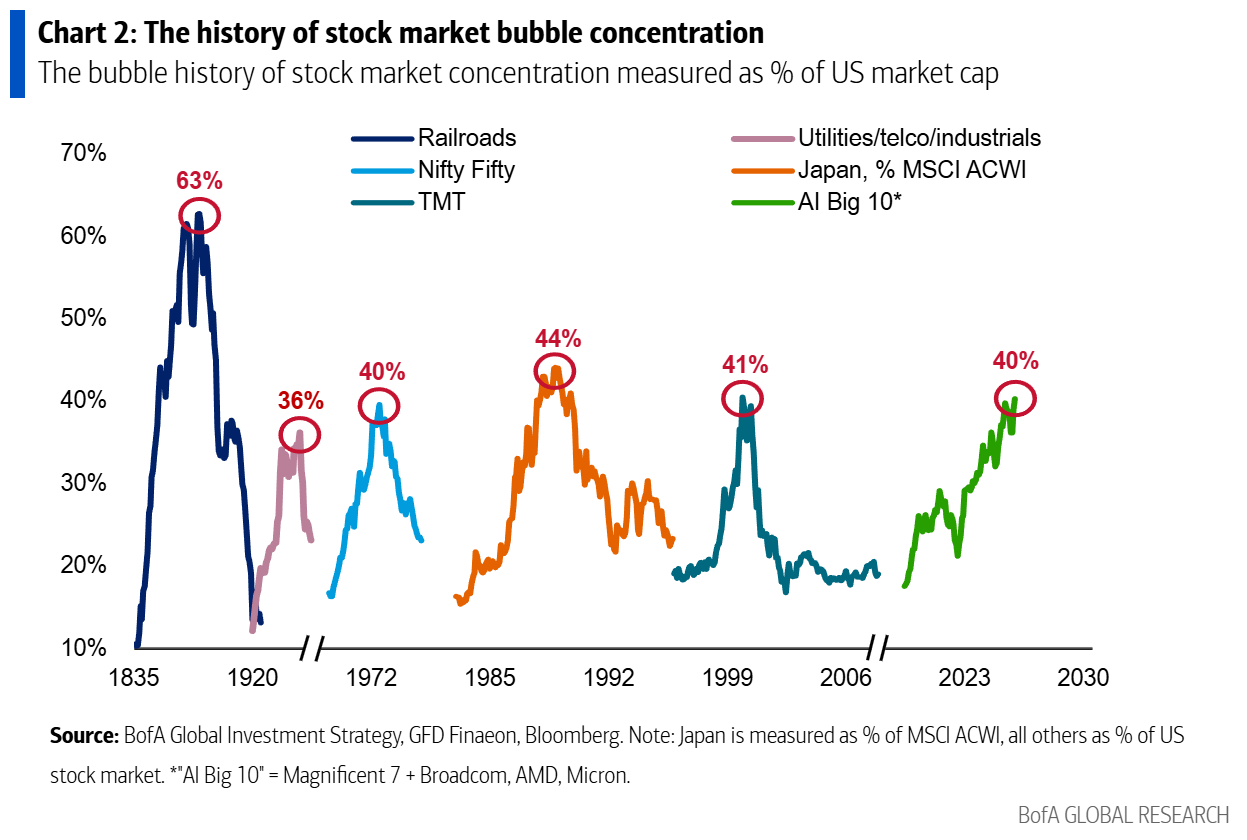

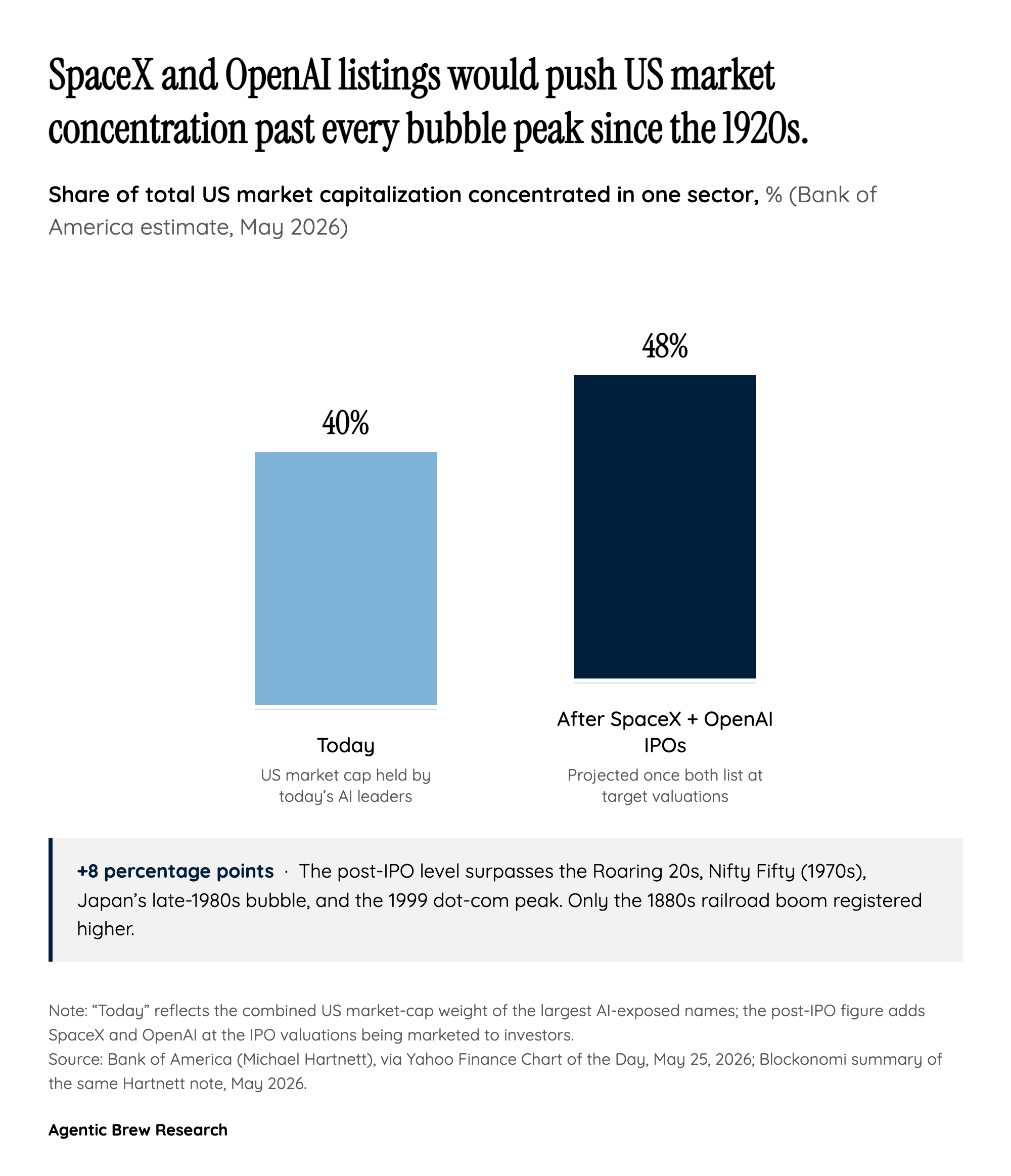

The 48% Number That Reframes the Whole Trade

Bank of America's Michael Hartnett ran a straightforward exercise — what happens to US market structure if SpaceX and OpenAI list at the valuations being marketed — and produced a number that has reset the bull-bear conversation. AI-related names currently account for roughly 40% of total US market capitalization. Adding the two new mega-caps at their target valuations pushes that share to about 48% [1]. The Roaring 20s, the Nifty Fifty of the early 1970s, Japan's late-1980s asset bubble, and the 1999 dot-com peak all registered lower single-sector concentration than that. The only episode in modern US history that registered higher was the 1880s railroad boom [2].

What makes the number more than trivia is what Hartnett's archive of comparable episodes shows next. Concentration peaks like these have historically been mean-reverting — sometimes slowly, sometimes via violent multi-year drawdowns. The bear case is not that AI as a technology is wrong; it is that when one sector controls almost half the index, every macro headwind transmits to portfolios as a single-factor shock, and the diversification baked into a broad-market fund quietly stops working. For an investor whose default exposure is the S&P 500, the SpaceX-OpenAI IPO wave is the moment 'the AI trade' and 'the market' become the same trade.