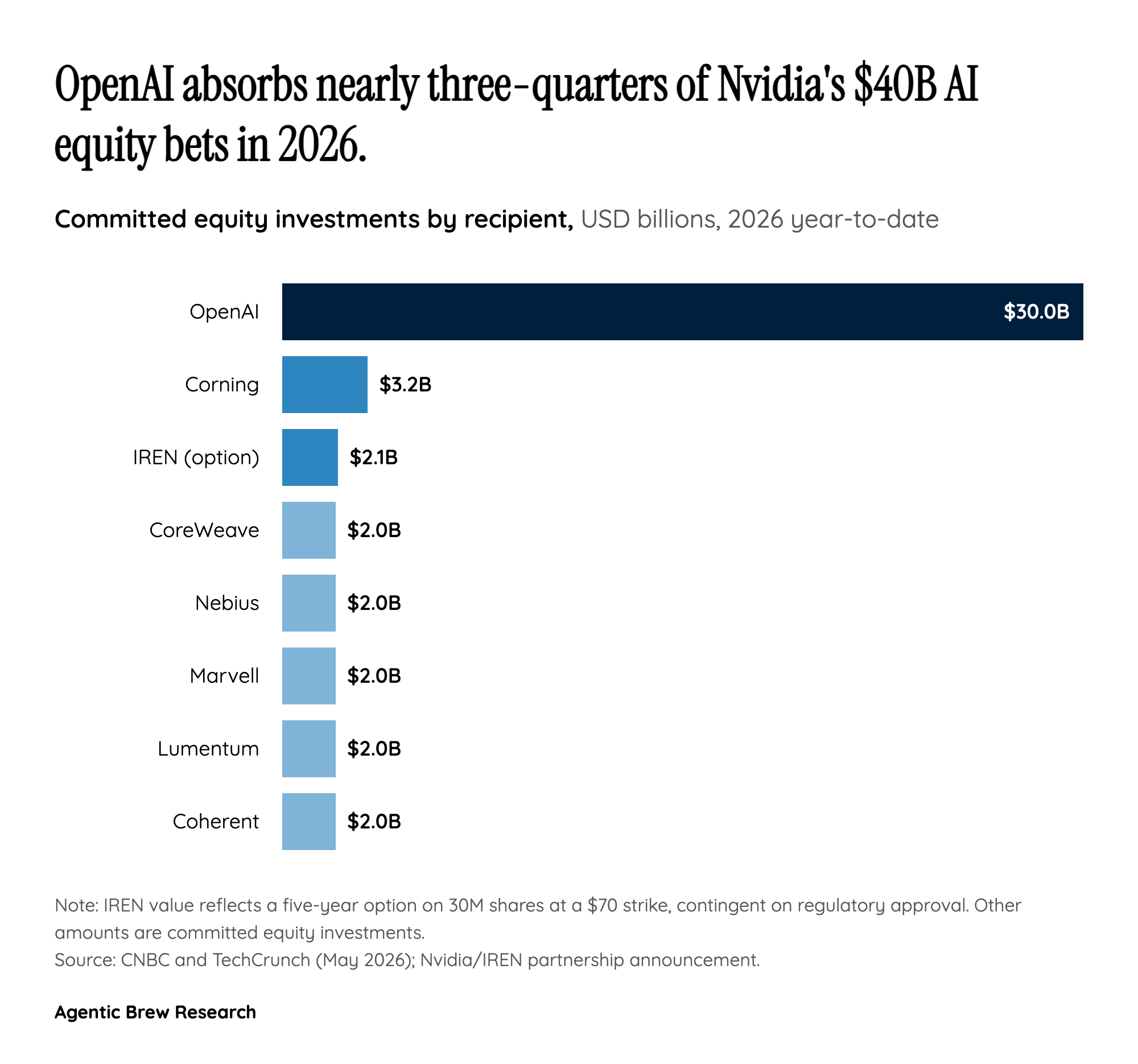

The Dual-Instrument Deal: Cash Today, Optionality Tomorrow

Strip the IREN announcement down to the wiring and you find two financial instruments stapled together. The first is a five-year, $3.4 billion managed GPU cloud services contract — concrete revenue, served on air-cooled Blackwell systems inside roughly 60MW of IREN's existing Childress, Texas campus. That's the cash leg, and it's what gives IREN the credit profile to keep building. The second is a five-year option for Nvidia to buy up to 30 million IREN shares at a $70 strike, a potential $2.1 billion equity stake that is contingent on regulatory approval. That's the equity leg, and it is structured as a warrant-like right rather than an obligation.

The asymmetry here is the story. Nvidia pays nothing today for upside in IREN's stock yet anchors itself as IREN's most strategic customer for half a decade. If IREN executes — building toward the planned 2-gigawatt Sweetwater campus and the broader 5GW DSX-aligned footprint — Nvidia exercises and captures the rerating. If IREN stumbles, Nvidia walks away from the option and still owns the cloud contract economics. Reddit's IREN community caught this dynamic immediately, with one widely upvoted comment framing it as Nvidia receiving 'a risk-free 5-year call option' while IREN holders absorb the dilution risk.