Why both labs imported Palantir's forward-deployed engineer model

The structural choice underneath both announcements is that Claude and GPT cannot, on their own, walk into a mid-sized insurer or a regional manufacturer and rewire its workflows. That work requires engineers who understand both the model and the customer's data plumbing — the role Palantir invented in the early 2010s when it embedded 'Delta' engineers inside intelligence-agency customers. That model is now being copied by Anthropic and OpenAI almost line-for-line, because the bottleneck to AI adoption has shifted from model quality to deployment labor.

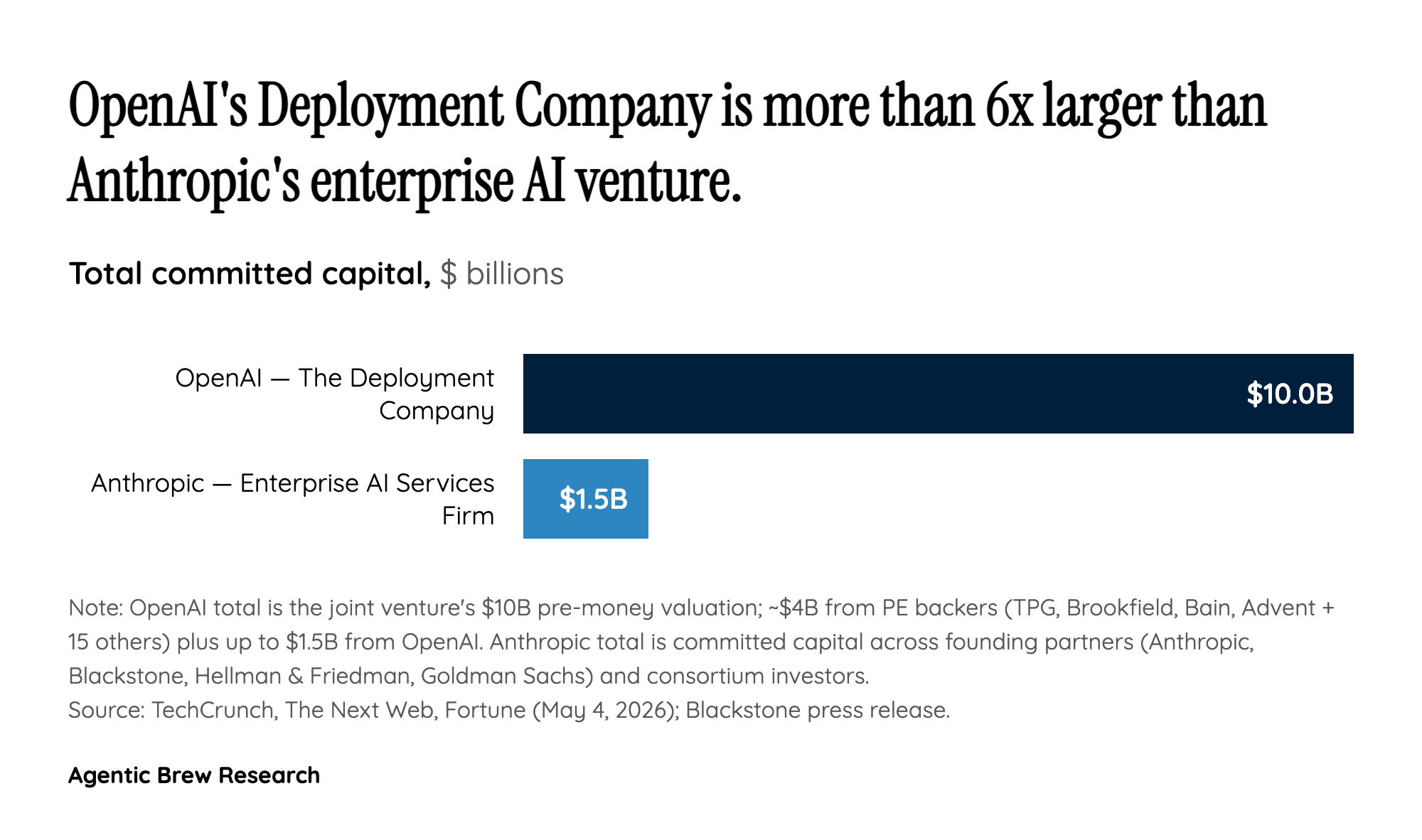

This is what Anthropic CFO Krishna Rao means when he says enterprise demand for Claude is significantly outpacing any single delivery model, and what Blackstone's Jon Gray identifies as the most significant bottleneck to enterprise AI adoption. The implication is unflattering for the model labs: shipping a frontier model is no longer a sufficient business. Without an embedded engineering layer, a customer signs a license, fails to operationalize it, churns, and the lab loses both revenue and reference value. By owning the FDE layer through these JVs, Anthropic and OpenAI capture the implementation work that would otherwise leak to consultants — and they do it with PE money rather than their own headcount.