How the Loop Actually Closes

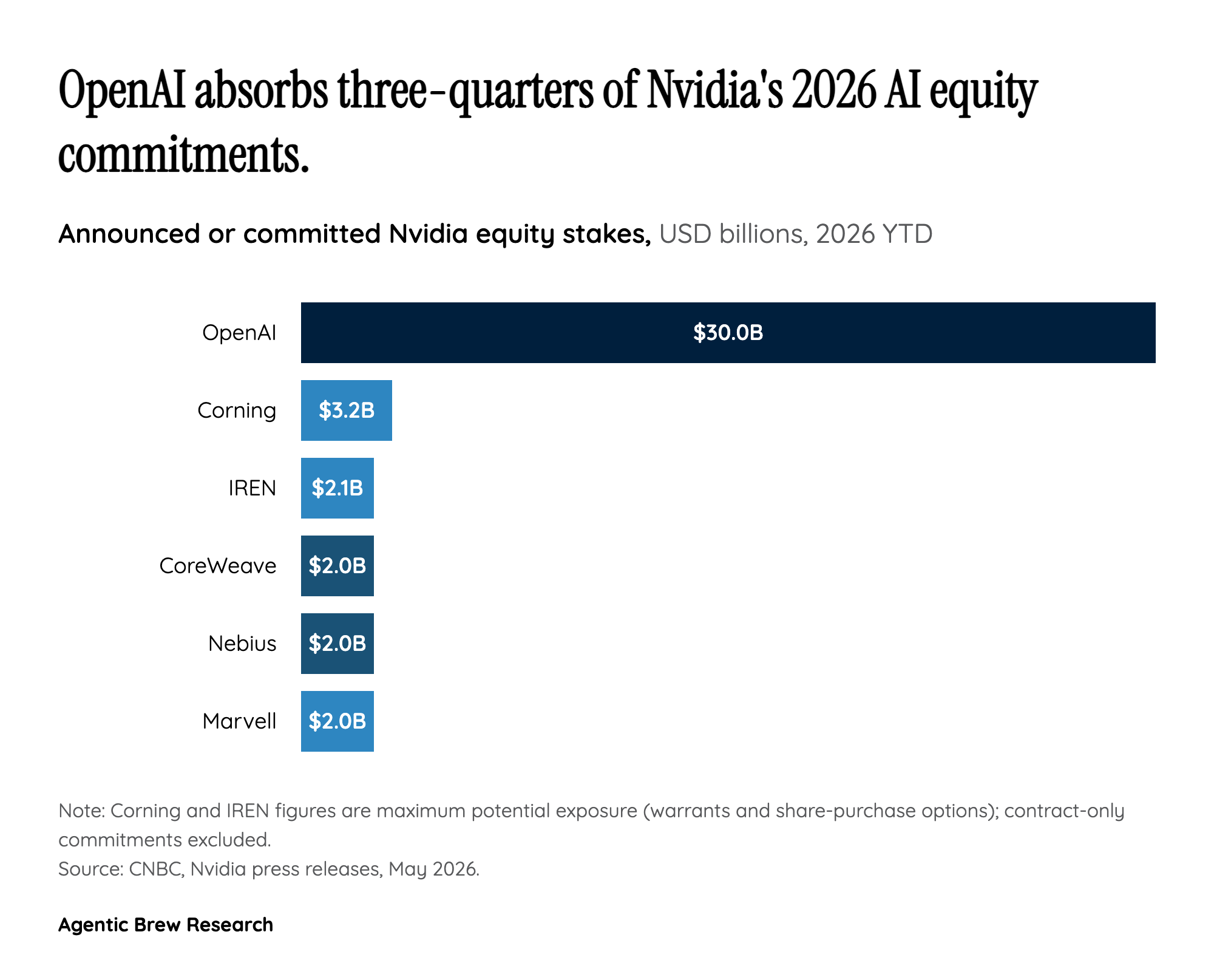

The standard read on Nvidia's 2026 spree — that the company is 'investing in AI customers' — undersells how tightly the deals are wired together. Each major neocloud arrangement bundles three instruments: an equity stake, a multi-year capacity-purchase or managed-cloud contract, and a deployment commitment denominated in gigawatts of Nvidia-aligned infrastructure. The CoreWeave package is the cleanest illustration: $2B of Nvidia equity in January paired with a $6.3B capacity-purchase agreement [1]. The IREN deal, announced May 7, follows the same template — a $3.4 billion five-year AI cloud contract sitting next to the right to buy 30 million IREN shares at $70 each, with both halves anchored to up to 5 gigawatts of DSX-aligned buildout [2].

What closes the loop is the direction of dollar flow inside that bundle. Nvidia writes the equity check; the partner uses fresh capital (plus the credibility the stamp confers in the debt markets) to fund GPU procurement and the power, land, and permits required to deploy them; Nvidia recognizes the chip revenue; the partner's enterprise value rises with the deployment milestones, marking the equity stake higher on Nvidia's balance sheet. Mizuho's Jordan Klein puts it plainly: 'It smells like you are pre-funding the purchase of your own GPUs and products' [1]. Nvidia's official rebuttal — that customers pay within 53 days and the business is economically sound [3]— addresses the accounting question but not the structural one, which is whether organic demand alone would have funded this much capacity at this speed.