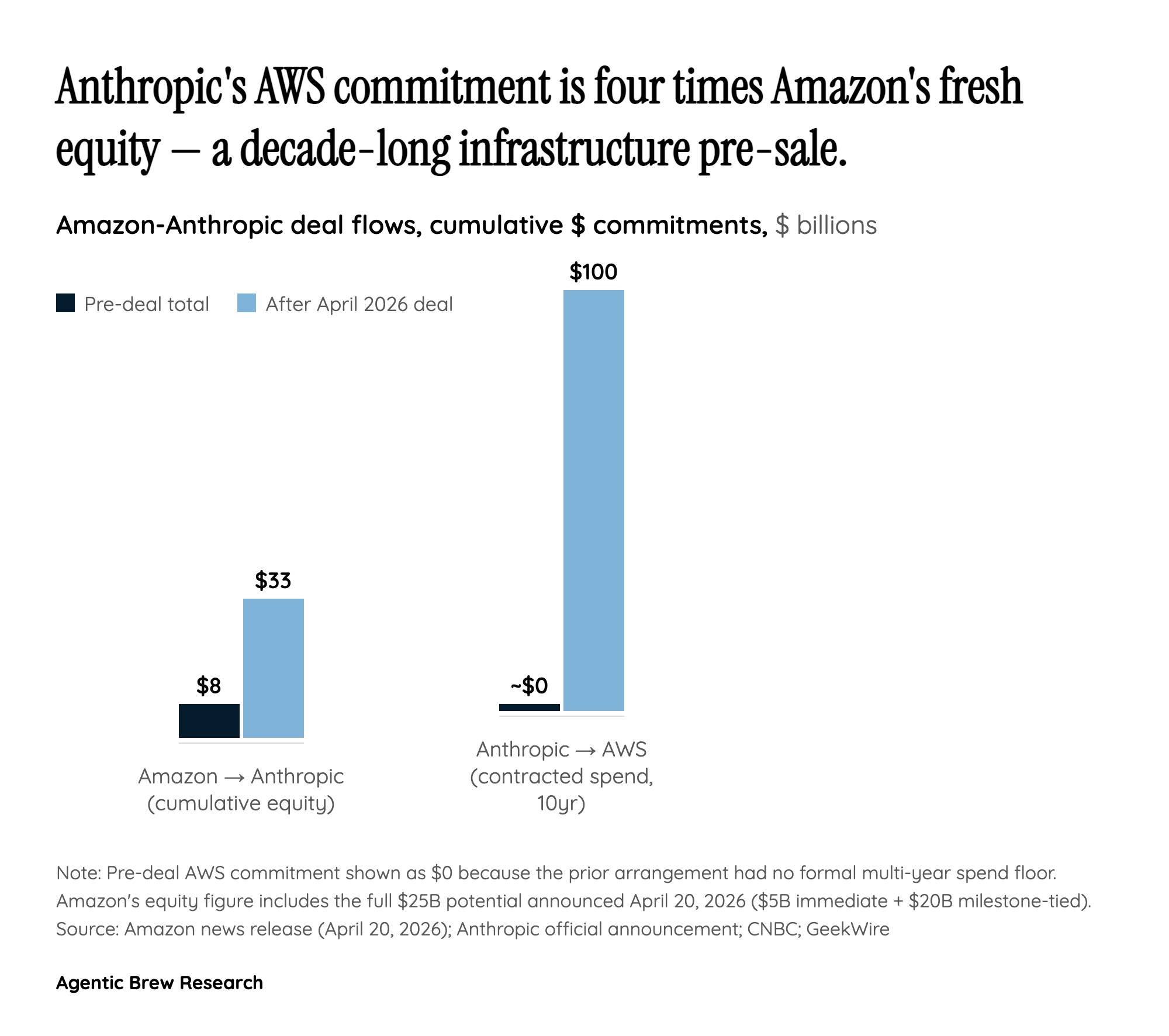

The 4:1 Spend-to-Equity Ratio: This Is a Pre-Paid AWS Contract Dressed Up as Venture Capital

The single most consequential thing about this deal is the asymmetry of its two legs. Amazon commits up to $25B of fresh equity — on top of $8B already on the books — at Anthropic's $380B Series G valuation. Anthropic, in turn, commits to spend more than $100B on AWS over the next ten years. Even using the cumulative $33B Amazon figure rather than just the new money, the ratio is roughly 3:1 in cash out to contracted revenue in, and closer to 4:1 if you weight only the $25B incremental tranche. Seen that way, this is not a venture investment in the traditional sense; it is a decade-long infrastructure pre-sale where Amazon funds a strategic customer so that customer can buy AWS capacity back from it.

That framing explains why finance-Twitter has zeroed in on the 'payback mechanism' angle and why r/StockMarket is openly skeptical about circular AI vendor financing. Evgeniy Mikhalevich argues the deal is structured to make Amazon's AI capex 'look strategically inevitable,' and The Decoder flags the open sustainability question: the math only works if AI revenue keeps pace with the spending both sides have now contractually promised. Jim Cramer's rebuttal — 'Isn't it possible that everyone wins?' — is the optimistic read, but it doesn't dispute the structure, just its implications. Either way, the financial press has quietly stopped calling this a venture investment.