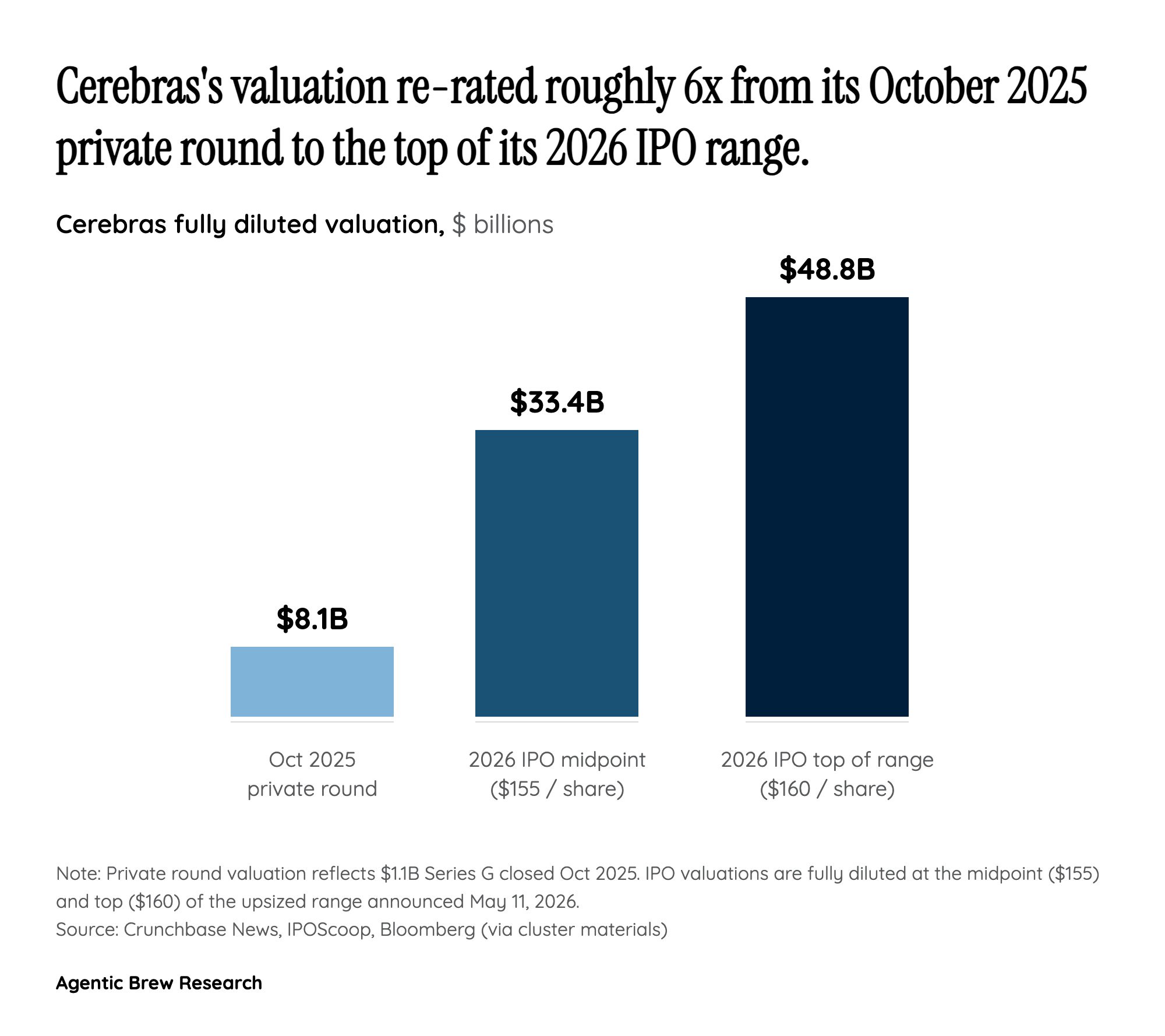

The Bookbuilding Mechanism: How 20x Demand Repriced the Deal in Days

In a normal IPO, bookbuilding is a slow tide: underwriters set an initial price range, road-show the deal for two weeks, gauge institutional interest, and price near the midpoint on listing eve. Cerebras has done something different. The original terms — 28 million shares at $115-$125 — would have raised roughly $3.5 billion [1]. Within days, indications of interest from institutions exceeded the available float by more than 20 times [2]. That kind of cover ratio is what underwriters call a 'multiple-times-oversubscribed' book; when it crosses 10x it typically triggers an upsize, and when it crosses 20x it forces a meaningful repricing because allocators are signaling they would accept a materially higher clearing price. Joint book-runners Morgan Stanley, Citigroup, Barclays, and UBS responded by lifting the range to $150-$160 on 30 million shares, raising the targeted proceeds to approximately $4.8 billion [1][3].

What 20x oversubscription actually means in practice is that for every share offered, more than twenty shares' worth of orders were submitted at or above the indicated price. That does not mean every order is firm at the new top of range — some orders are conditional, some get cut on allocation — but it does mean the bankers have very high confidence the deal will clear at $160 and that aftermarket appetite is real. The flip side, and the reason sophisticated investors are paying attention to the cadence, is that lifting both the share count and the price range in such a compressed window is unusual. It suggests either that the original range was deliberately conservative to manufacture momentum, or that the demand environment is moving so fast that underwriters are repricing in near-real time. Either reading carries implications for how the stock trades when CBRS is expected to list on Nasdaq [4].