The $40B Loop That Pays Itself Back

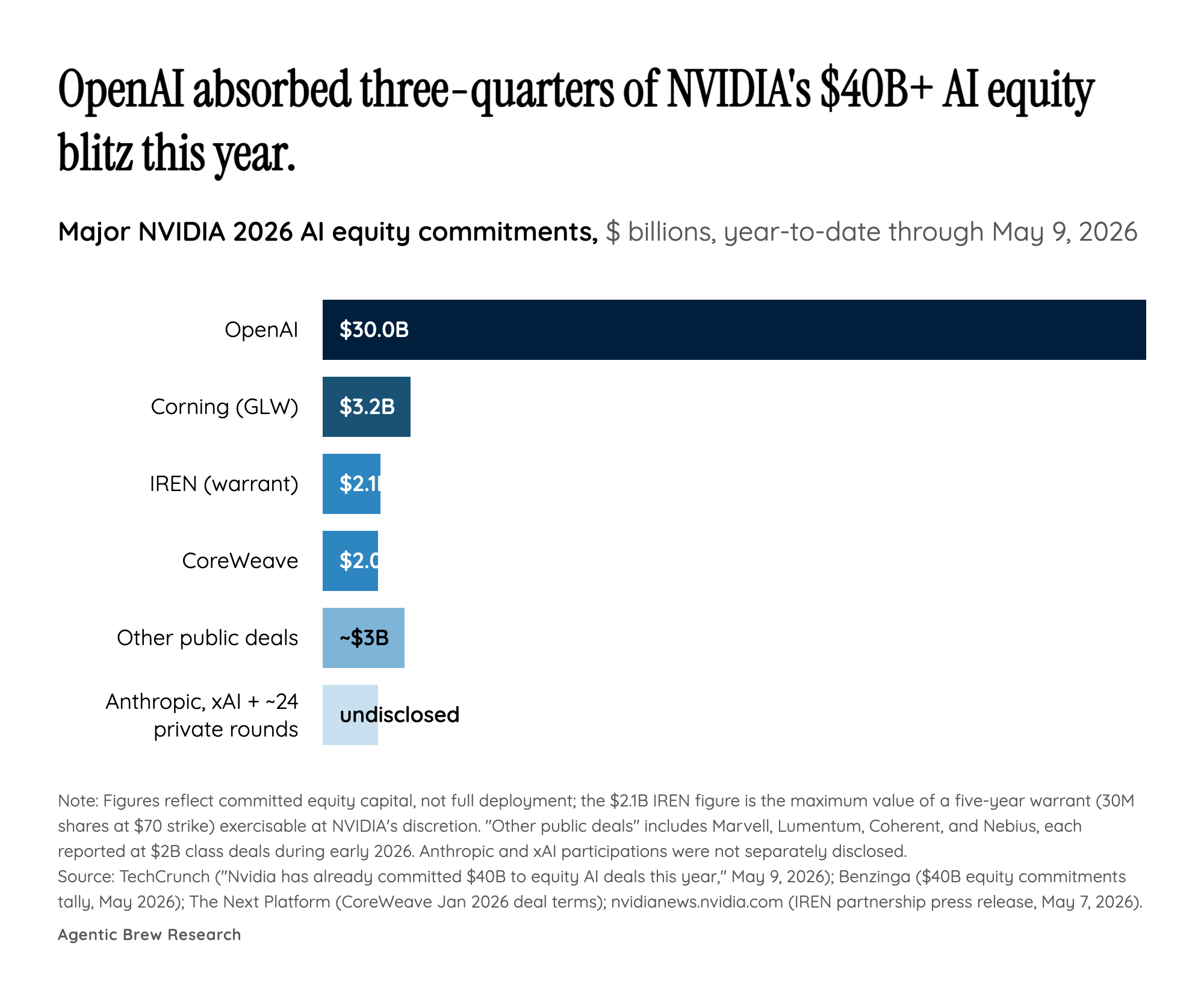

The arithmetic of NVIDIA's 2026 capital strategy is what makes it both extraordinary and contested. In roughly four months, NVIDIA committed more than $40 billion in equity to the AI ecosystem: roughly $30 billion into OpenAI, $2 billion into CoreWeave at $87.20/share (lifting its stake to ~13%) with a $6.3 billion expanded master services agreement through 2032, up to $3.2 billion into Corning for optical interconnects, up to $2.1 billion in IREN warrants at a $70 strike, and a ~$5 billion Intel stake that has reportedly already swelled to over $25 billion. Each of those recipients is, in turn, either a direct customer for NVIDIA chips (OpenAI, CoreWeave, IREN, Anthropic via CoreWeave) or a supplier to the NVIDIA-anchored AI factory (Corning, Intel).

That is the mechanical basis for the 'circular investment' critique. As one widely upvoted Reddit framing put it, if the entire $40 billion eventually cycles back as chip orders, roughly a fifth of NVIDIA's revenue would be funded from its own balance sheet — a structural argument independent of any single deal. NVIDIA's official rationale, delivered cleanest by CFO Colette Kress on earnings calls, narrows the claim: the equity stakes exist to ensure 'compute capacity is being built around its hardware,' not to inflate revenue. In that telling, each check is a supply-securing instrument — IREN's warrant only converts to cash if gigawatts get built; CoreWeave's MSA is sized to actual capex absorption; the Corning and Intel stakes lock in upstream optics and fab capacity. The mechanical loop and NVIDIA's defense are two readings of the same arithmetic; the gap between them is exactly the analytical question dominating sell-side desks this week.