The 80-Second Window That Re-Rated AI Capex by $55 Billion

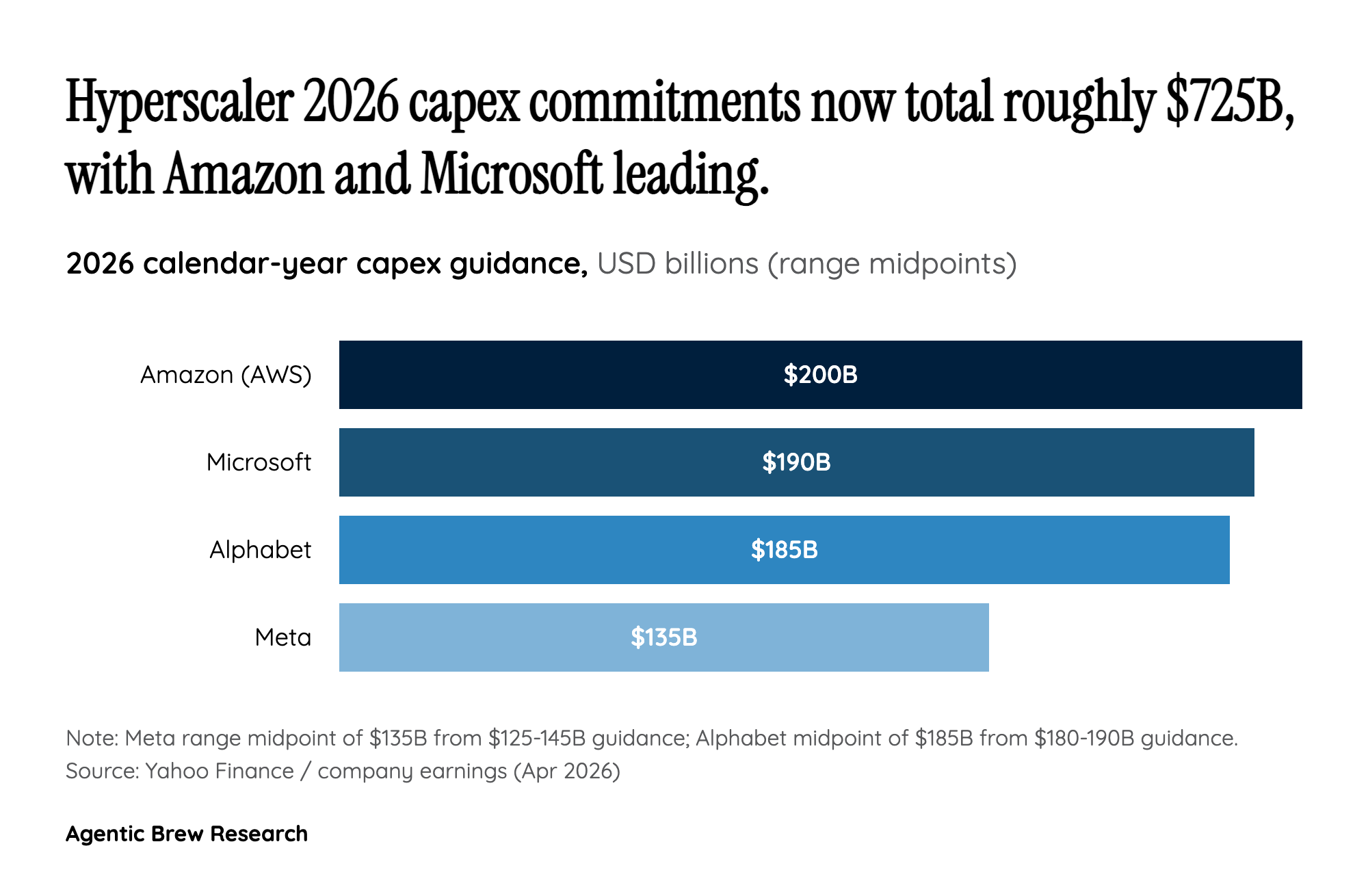

Big Tech's earnings cluster on April 29, 2026 was choreographed almost to the second — Bloomberg called the moment when Alphabet, Meta, Microsoft, and Amazon prints landed inside a roughly 80-second window the night that 'will decide the stock market's fate.' Inside that window, the high-end consensus estimate for 2026 hyperscaler AI capex jumped from around $670B to roughly $725B. That is a $55B re-rating, larger than the entire annual capex of every non-hyperscaler in the S&P 500 except a handful of utilities, absorbed by the market in real time.

The drivers were specific. Microsoft guided to $190B for calendar 2026, explicitly flagging $25B of that as the cost of higher GPU and component pricing rather than incremental capacity. Alphabet raised both ends of its range by $5B to $180-190B. Meta lifted its band by $10B at both ends to $125-145B. Amazon stayed near the top of the pack at roughly $200B. The takeaway is that 'AI capex' is now structurally a four-handed bid into a constrained component supply chain — every hyperscaler is signaling they would rather build ahead of demand than risk being short of GPUs in 2027, which is why the line went up at all four companies on the same night.