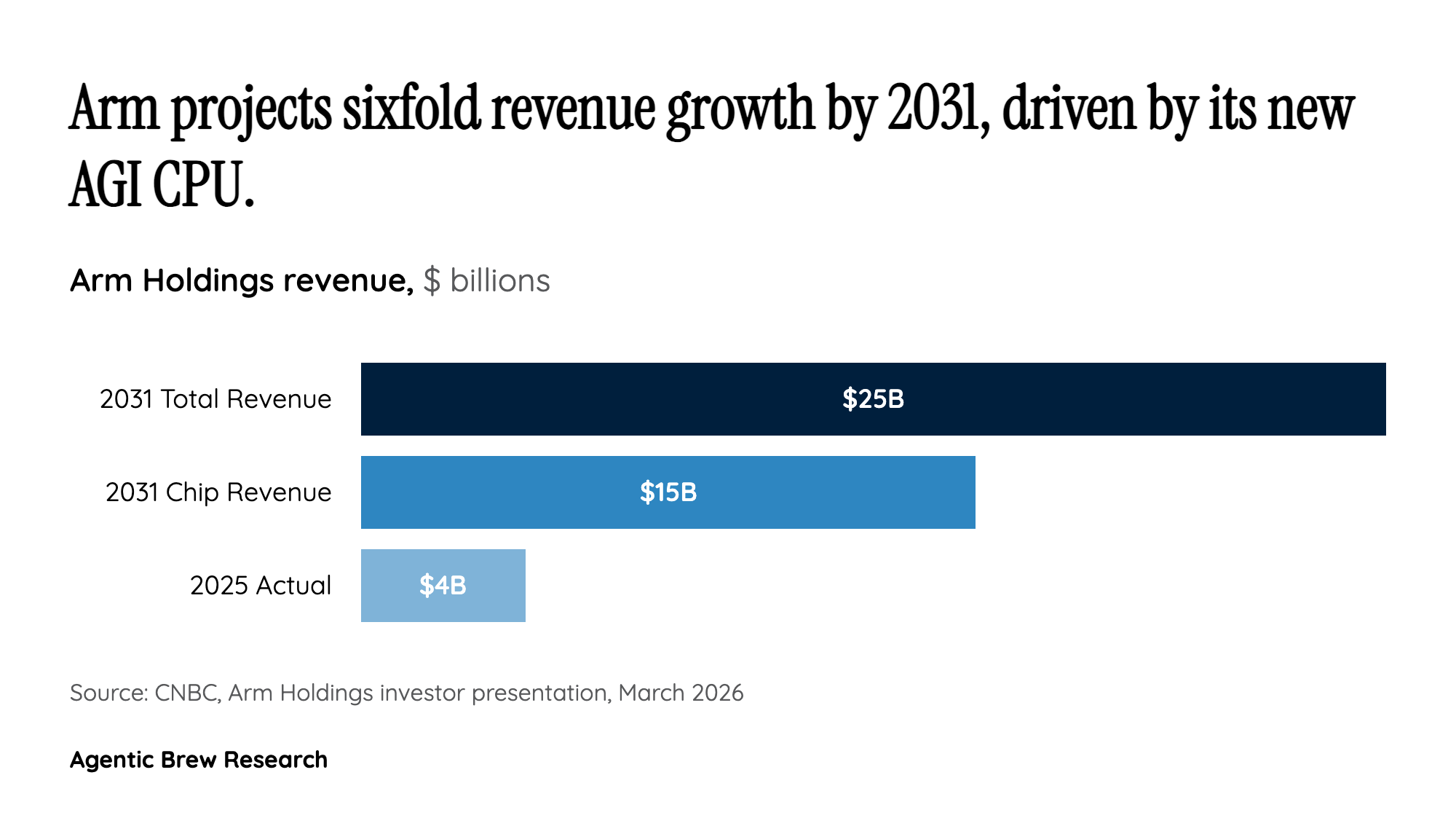

Why This Matters

Arm's decision to design and sell its own data center CPU represents the most consequential strategic pivot in the semiconductor industry in decades. For 35 years, Arm operated as a pure IP licensor, collecting royalties of roughly 1-2% on every chip built using its architecture. That model made Arm ubiquitous — its designs power virtually every smartphone on the planet — but it also left enormous value on the table as hyperscalers began spending hundreds of billions on AI infrastructure. By shipping its own silicon, Arm can now capture full chip margins estimated at around 50% gross profit, a transformative uplift from the thin royalty streams of its licensing business.

The timing is not accidental. The AI infrastructure buildout is creating unprecedented demand for energy-efficient compute, and Arm's RISC-based architecture holds an inherent power efficiency advantage over x86. With hyperscalers like Meta planning $115-135 billion in AI capital expenditure, even a small share of that spending translates into billions in new revenue for Arm. Citi analysts called it 'the most significant shift in the company's history,' and the market agreed — Arm stock surged 13% premarket as investors repriced the company from a licensing business to a potential chip powerhouse.