Why This Matters

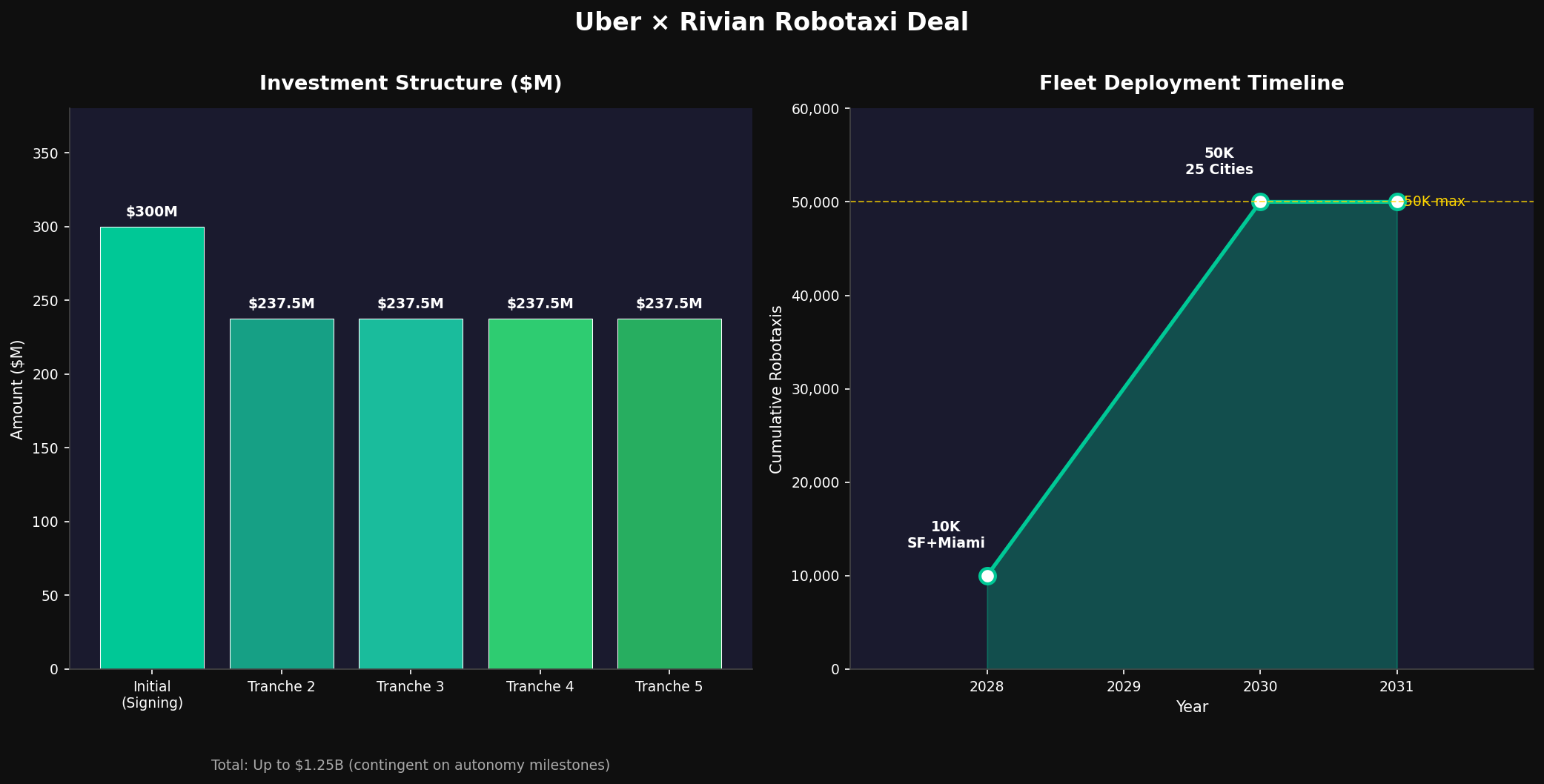

The Uber-Rivian deal represents a structural shift in how the autonomous vehicle industry is being financed and distributed. Rather than building its own AV fleet or acquiring AV technology outright, Uber is acting as a capital allocator and distribution guarantor providing the demand certainty that AV developers need to justify enormous R&D expenditures. By committing up to $1.25B across milestone-gated tranches, Uber secures exclusive robotaxi supply while shifting technology execution risk onto Rivian. This is the same playbook executed with Waabi at $1B for 25,000 vehicles in January 2026 and mirrors Uber post-ATG strategy of partnering rather than building.

For Rivian, the deal is existential in its ambition. Abandoning the 2027 EBITDA-positive target on the same day signals that management has explicitly chosen the long-arc autonomy bet over near-term financial stability. With Rivian burning approximately $86,000 per delivered vehicle in 2025, the $1.25B in committed capital and the guaranteed 50,000-unit demand floor materially changes the unit economics calculus provided autonomy milestones are hit. The deal also validates Rivian controversial decision to build its own RAP1 chip and software stack rather than licensing from Mobileye, Waymo, or another third party.