The Nasdaq Shell Arbitrage: Why the Ticker Is the Product

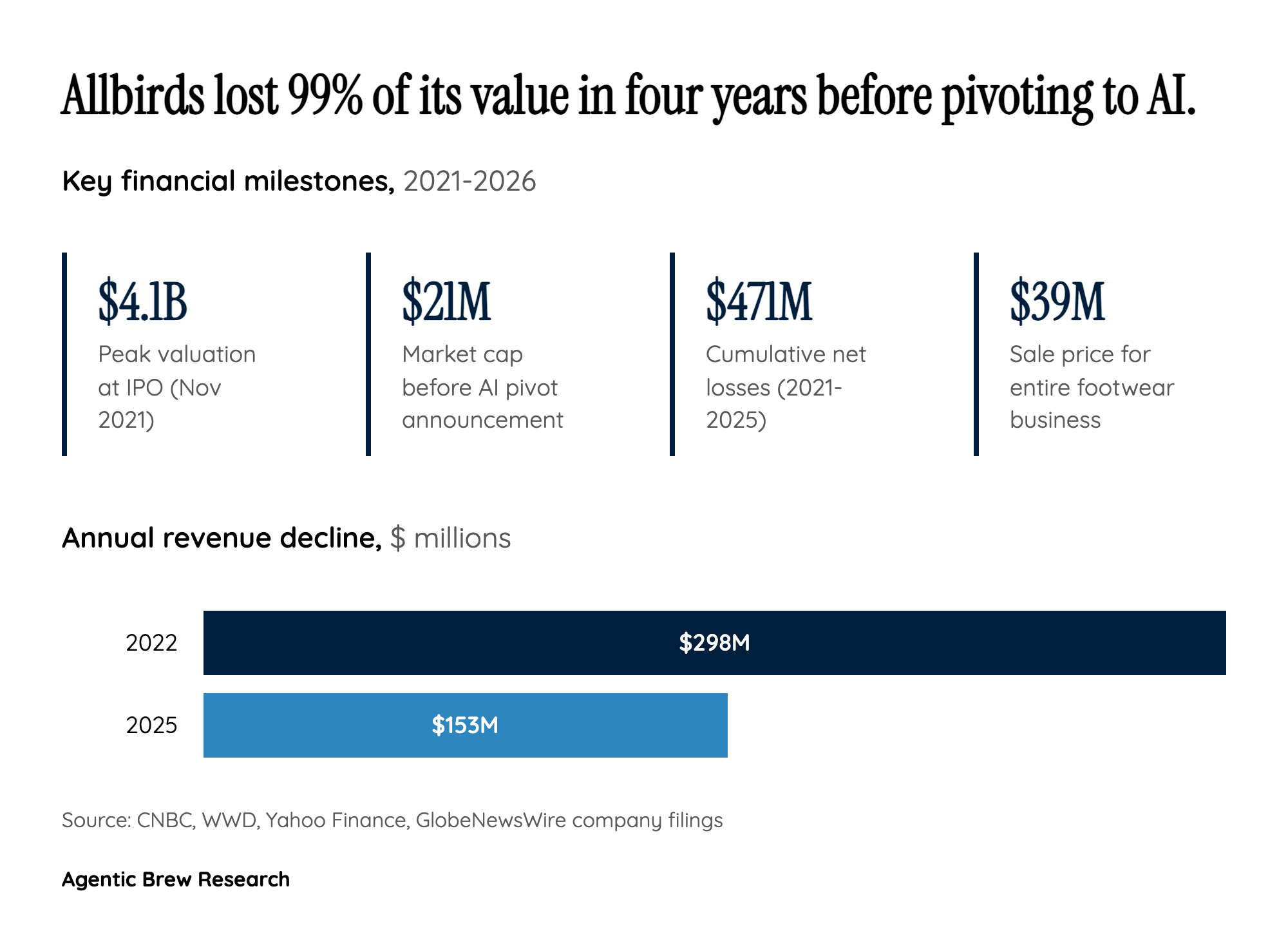

The most important thing to understand about the NewBird AI pivot is that it is not really about AI infrastructure. It is about the value of a publicly traded shell. Taking a company public through a traditional IPO costs tens of millions of dollars in legal fees, underwriting, and compliance work, and takes 12-18 months. A company that already has a Nasdaq listing, SEC reporting infrastructure, and public market access can skip all of that. Allbirds, stripped of its footwear business, is essentially a clean public vehicle with roughly $39 million in incoming cash from the American Exchange Group sale and a $50 million financing commitment.

This is why the stock surged 700% despite the company having zero AI capabilities. Investors are not betting on NewBird AI's ability to compete with AWS, Azure, or CoreWeave in GPU leasing. They are betting that a Nasdaq-listed entity with fresh capital and a hot-sector narrative will attract speculative interest, potential reverse merger partners, or further financing. The company's decision to retain the ticker symbol BIRD — rather than changing to something AI-related — is itself revealing. The brand equity, such as it is, lives in the listing. The $21 million pre-announcement market cap made this an unusually cheap vehicle, and the convertible financing structure means the unnamed institutional investor likely negotiated significant equity upside, potentially diluting existing shareholders substantially.