The Day the AI Trade Stopped Being a GPU Trade

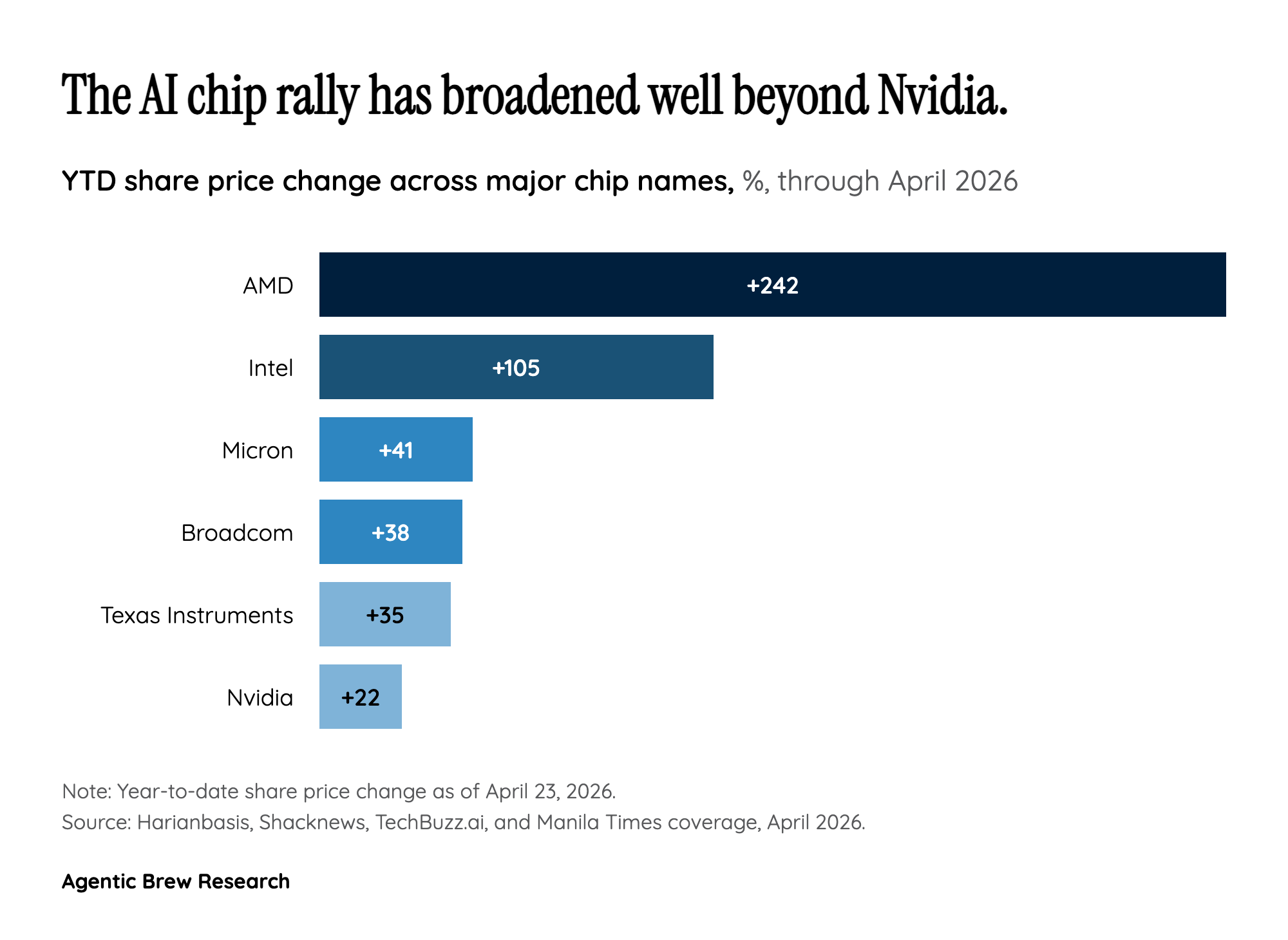

For most of the generative-AI cycle, 'AI capex' has effectively been shorthand for 'Nvidia.' April 23, 2026 is the day that story broke open. Texas Instruments, a 94-year-old analog house best known for op-amps, power-management ICs, and calculators, posted 19% revenue growth and guided Q2 revenue to $5.0-5.4B versus a $4.86B consensus — and the stock jumped 19% for its best single day since 2000. The reason isn't a new GPU architecture. It's that every AI server rack the hyperscalers build needs dense arrays of TI's voltage regulators, signal-conversion chips, and interface parts. TI's CEO Haviv Ilan put a number on it: the data center segment grew 'around 90 percent from the same period last year,' and is now a >$1B annual revenue business layered on top of an industrial base that is itself recovering from a multi-year downcycle.

Intel's print reinforces the same thesis from the other side of the chip. The Data Center and AI segment hit $5.1B, up 22% YoY and ~$700M above consensus, and CFO David Zinsner specifically attributed the beat to 'the growing and essential role of the CPU in the AI era.' That framing would have been laughed off in 2023. In 2026 it's the beat. Put the two earnings together and the market read is unambiguous: AI capex is spilling out of the GPU silo and into analog, CPUs, advanced packaging, and interconnect — the full bill of materials for an AI data center, not just its accelerator. That's why the Philadelphia Semiconductor Index crossed 10,000 for the first time on the same day these two companies reported. The rally is broadening, not narrowing.