By The Numbers: How Cerebras Priced Itself Past Nvidia

The mechanics of the Cerebras IPO are the story. The company marketed shares at $150-$160, priced at $185 — well above the top of the range — and still saw orders exceed available shares by more than 20x, forcing it to upsize both the share count and the price range twice during the roadshow [1]. That is institutional desperation, not enthusiasm. By the time CBRS opened on Nasdaq it printed $350 (+89%), peaked intraday near $385 (+108%), and closed at $311.07 — up 68.2% on the day, with the market cap brushing $100 billion before settling near $66 billion at the close [2][3].

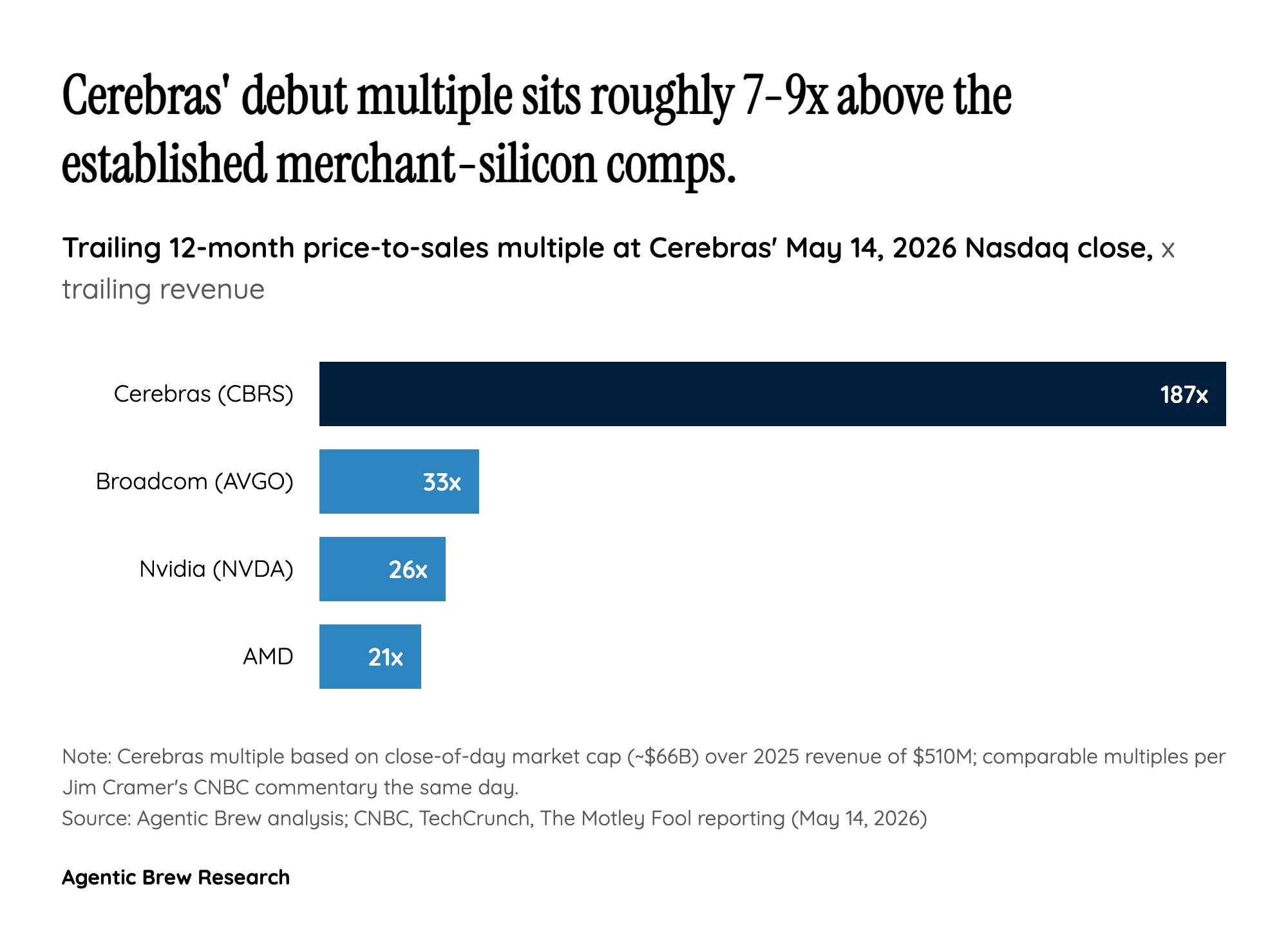

The valuation math is where the air gets thin. Cerebras booked $510M in 2025 revenue, up 76% year over year, but with a $145.9M operating loss. At a closing market cap near $66B, that's roughly 187x trailing sales — versus Nvidia at ~26x and AMD at ~21x. Jim Cramer called the multiple 'fanciful' on CNBC and said the action was 'right out of 1999,' explicitly telling viewers not to chase the stock [4]. D.A. Davidson, more sober, wrote that 'after reading the S1 and watching the roadshow, we wouldn't get too excited' [4].

The community on Reddit went further. One r/investing technical analyst noted that 2025 reported net income includes a $363.3M non-cash gain from a G42 forward contract — strip that out and Cerebras is at a $75.7M non-GAAP loss. By that lens the apparent profitability narrative is an artifact of the regulatory restructuring, not operating leverage. Shares fell roughly 10% the day after debut as those critiques surfaced in mainstream coverage [5].