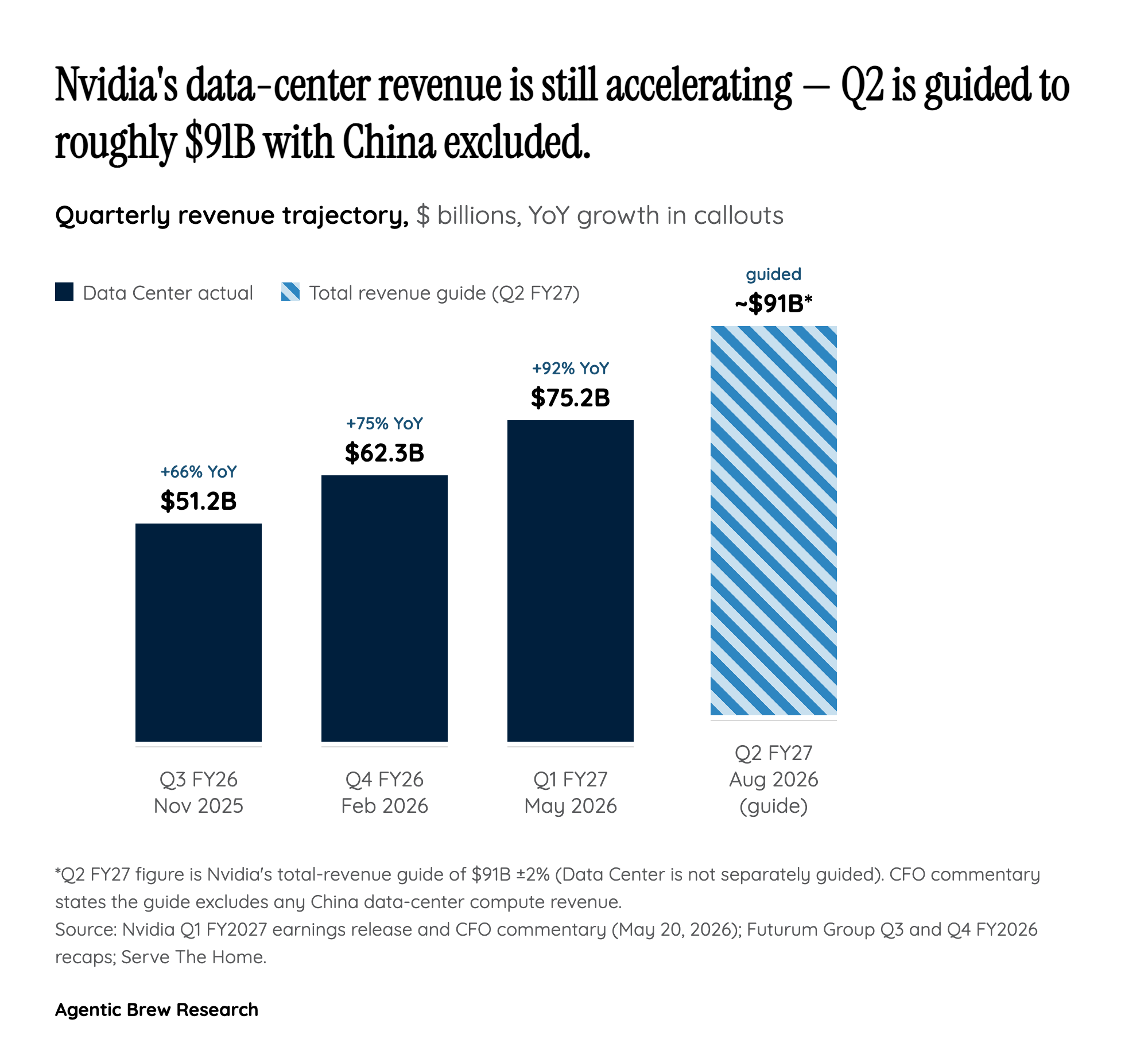

The Beat That Didn't Beat

On paper, this was the kind of print companies dream about. Revenue of $81.6B blew past a $79.2B consensus, data center alone hit $75.2B (up 92% YoY), Q2 was guided to ~$91B against an $86.8B Street estimate, and the board piled on an $80B buyback authorization plus a 25x dividend hike [1][2][3]. Free cash flow came in at $48.6B in a single quarter. The stock opened about 0.5% lower.

That reaction is the real story. As Kiplinger's roundup of sell-side notes laid out, Nvidia has now beaten revenue estimates by 3-4% for six consecutive quarters and still closed lower on four of the last five prints [4]. Daniel Newman of Futurum captured the dynamic precisely: 'Wall Street has pulled itself above the company's own guide for the first time in this cycle, which raises the bar for what counts as a beat' [4]. Capital.com's Kyle Rodda called it 'a garden variety beat... well telegraphed,' and Wedbush's Matt Bryson had warned beforehand that the open question was simply whether the stock could rally on a solid print at all [4]. The arithmetic of the buyback only sharpens the point — when management is willing to absorb $80B of its own shares plus $38.5B already authorized [5], and the market still shrugs, it is the buy-side bar, not the company, that has changed.