The Comeback Narrative vs. The Fine Print

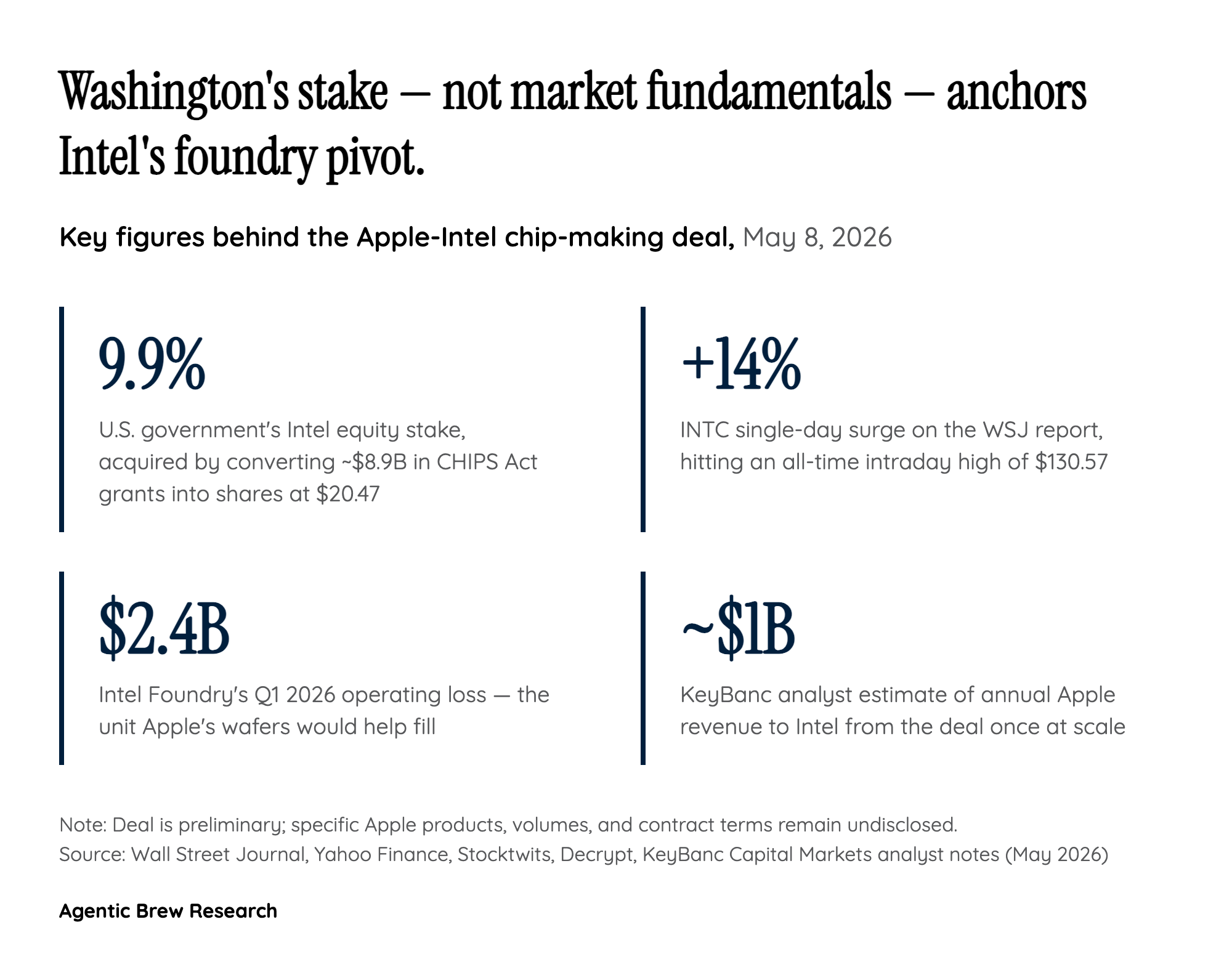

The market priced this as a homecoming. Intel jumped ~14-16% to an all-time intraday high of $130.57, the rally pulled the S&P 500 and Nasdaq to record closes, and r/wallstreetbets revived the legendary Intel YOLO mythos with $150-200 price targets. The story writes itself: Apple left in 2020, Intel rebuilt under Lip-Bu Tan, 18A finally hit high-volume manufacturing at Fab 52 in January 2026, and Apple is back.

The fine print tells a more measured story. KeyBanc's John Vinh says Intel landed Apple "on 18A for low-end M-series processors for MacBooks and iPads" targeting 2027, with 14A discussions for low-end iPhone A-series chips around 2029. WSJ sourcing did not specify which Apple products are covered, and Bloomberg notes Apple has not yet placed orders. The estimated $1 billion in annual revenue is meaningful for an Intel Foundry that posted a $2.4B operating loss in Q1 2026 — but it is not a flagship-product win. Apple Silicon's Pro and Max tiers, the iPhone Pro A-series, and anything that defines Apple's premium products remain anchored at TSMC.

This is a legitimately important validation for Intel Foundry. It is not the 2005 Intel-inside era returning. The honest read is closer to: Apple is opening a second source on its lowest-margin silicon, on a node Intel just brought online, in a deal whose volumes and timing remain undisclosed — and the market priced it like a strategic reunification.