The Q2 guide is the real catalyst — not the Q1 print

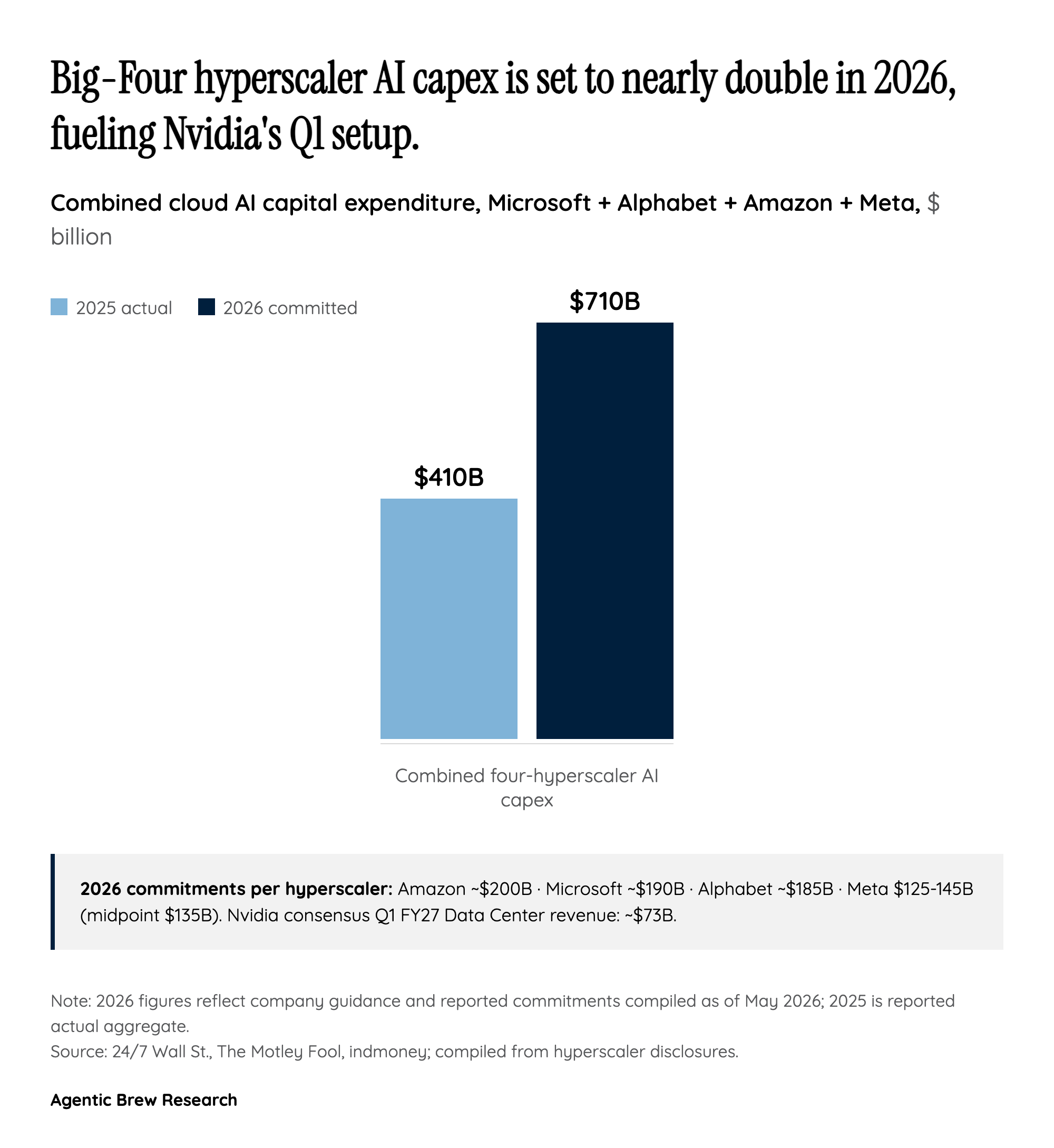

Almost nobody on the sell side expects Nvidia to miss Q1. The company guided $78.0B plus or minus 2% itself, consensus has migrated to ~$78.5-$78.8B with $1.77 non-GAAP EPS, Citi sees a $1.4B upside surprise to roughly $80B, and Polymarket is pricing a ~90% probability of a beat [1][2][3]. With that much of the result already discounted, the actual fight on May 20 is over the Q2 FY2027 outlook. Consensus sits at $85-$87B, but UBS's Timothy Arcuri raised his PT to $275 and explicitly told clients he expects a $90-$91B guide on the back of the Blackwell B300 ramp and an early Vera Rubin rack signal [4][5]. The Motley Fool's read is sharper: "Analysts are expecting forward revenue guidance of about $87 billion for Q2 2027. If the company's projections are higher, it's a strong signal that Nvidia remains at the center of the AI build-out" [1]. In other words, anything in the $85-87B range is a tie, and only a print starting with a 9 keeps the rally honest. The Data Center line, where consensus is ~$73B and Blackwell already drove close to 70% of data center compute revenue last quarter, will be the second number the market scans before it decides which way the after-hours tape goes [2][6].