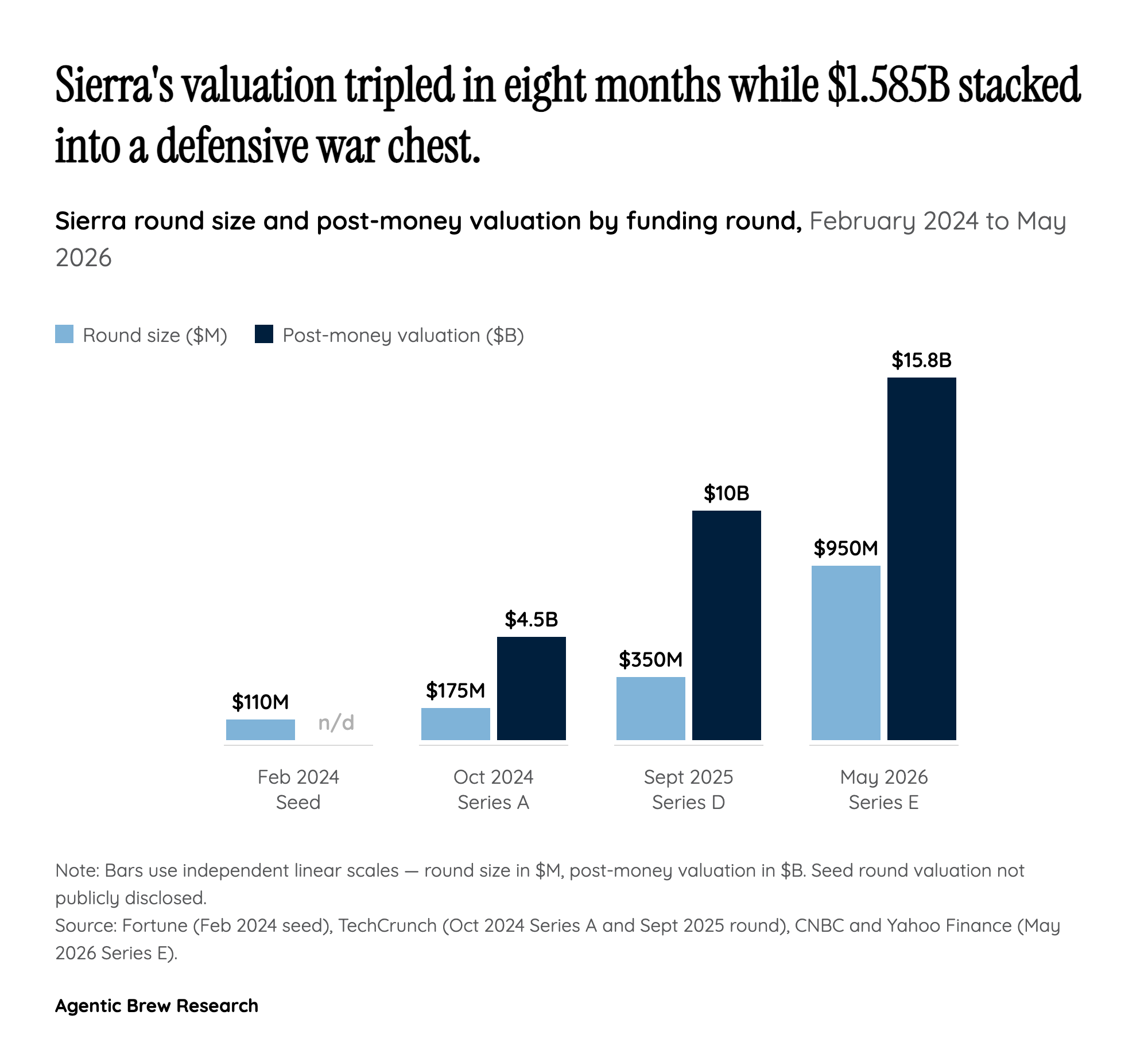

By the numbers: a 27-month capital stack and a 3.5x markup in eight months

Sierra's funding history reads less like a normal venture trajectory and more like a controlled escalation. February 2024: $110M from Sequoia and Benchmark out of stealth. October 2024: $175M led by Greenoaks at $4.5B. September 2025: $350M from Greenoaks again at $10B. May 2026: $950M co-led by Tiger Global and GV at $15.8B. That is roughly $1.585B raised across four rounds in 27 months, with the valuation marking up 3.5x in just eight months between September 2025 and May 2026.

What makes the curve unusual is not the size of any single round but the cadence — each round arrives before the previous one needs to be topped up, which is a deliberate signal. Sierra is not running out of money; it is choosing to take more, repeatedly. Bret Taylor was explicit that the capital is intended to widen Sierra's lead while it already exists, not to close a gap. Insider participation from Benchmark, Sequoia, and Greenoaks at every up-round also matters: those are the funds that price-discover Sierra's reality, and they have chosen each time to defend their positions at marks they themselves helped set, rather than letting new outside leads dilute them at lower entry points.