The compute ceiling is the real story: Google Cloud's growth is throttled by physics, not demand

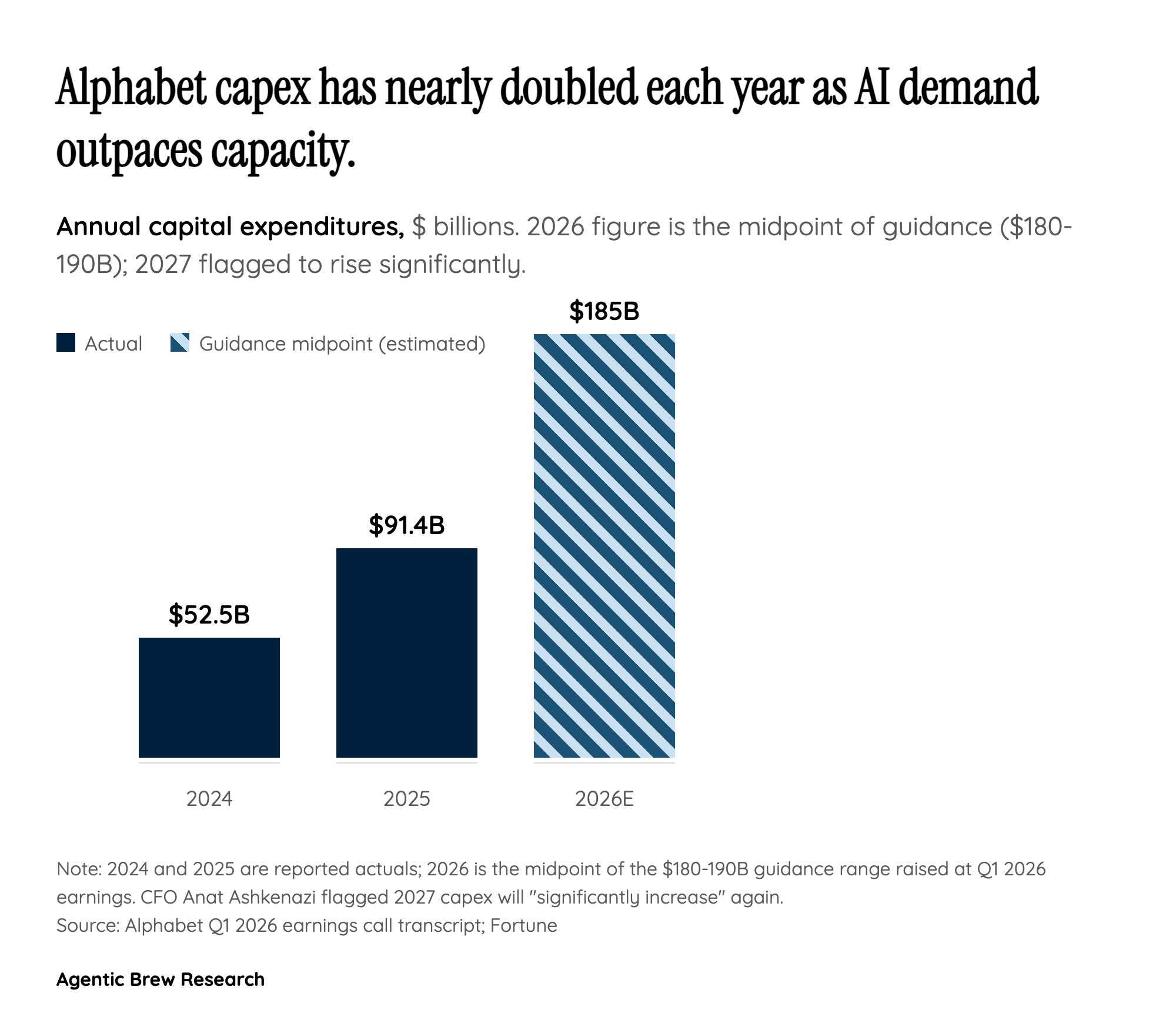

The number that should anchor any read of this print isn't the 63% Cloud growth rate or even the $20B run rate — it's the $462B backlog, which nearly doubled quarter-over-quarter from roughly $240B at the end of 2025. Pichai's admission that 'cloud revenue would have been higher if you were able to meet the demand' isn't boilerplate caution; it's a structural statement about a business where the binding constraint has shifted from sales motion to silicon, power, and concrete. Management said they expect to work through about half of the backlog over the next 24 months, which means roughly $230B of contracted revenue is sitting on the other side of capacity that doesn't yet exist.

That reframes the entire capex argument. When a hyperscaler tells the market it's spending $180-190B in a year, the instinctive question is 'what if demand doesn't show up?' Alphabet's answer is that demand has already shown up — it's been signed, contracted, and queued — and the risk is on the supply side: how fast can data centers, custom TPUs, networking, and energy interconnects actually be deployed. That's a fundamentally different risk profile than speculative buildout, and it's the lens through which the 2027 capex 'significant increase' guidance should be read. The buildout is multi-year because the backlog is multi-year.