Why Wall Street rewarded Alphabet and punished Meta for the same AI bill

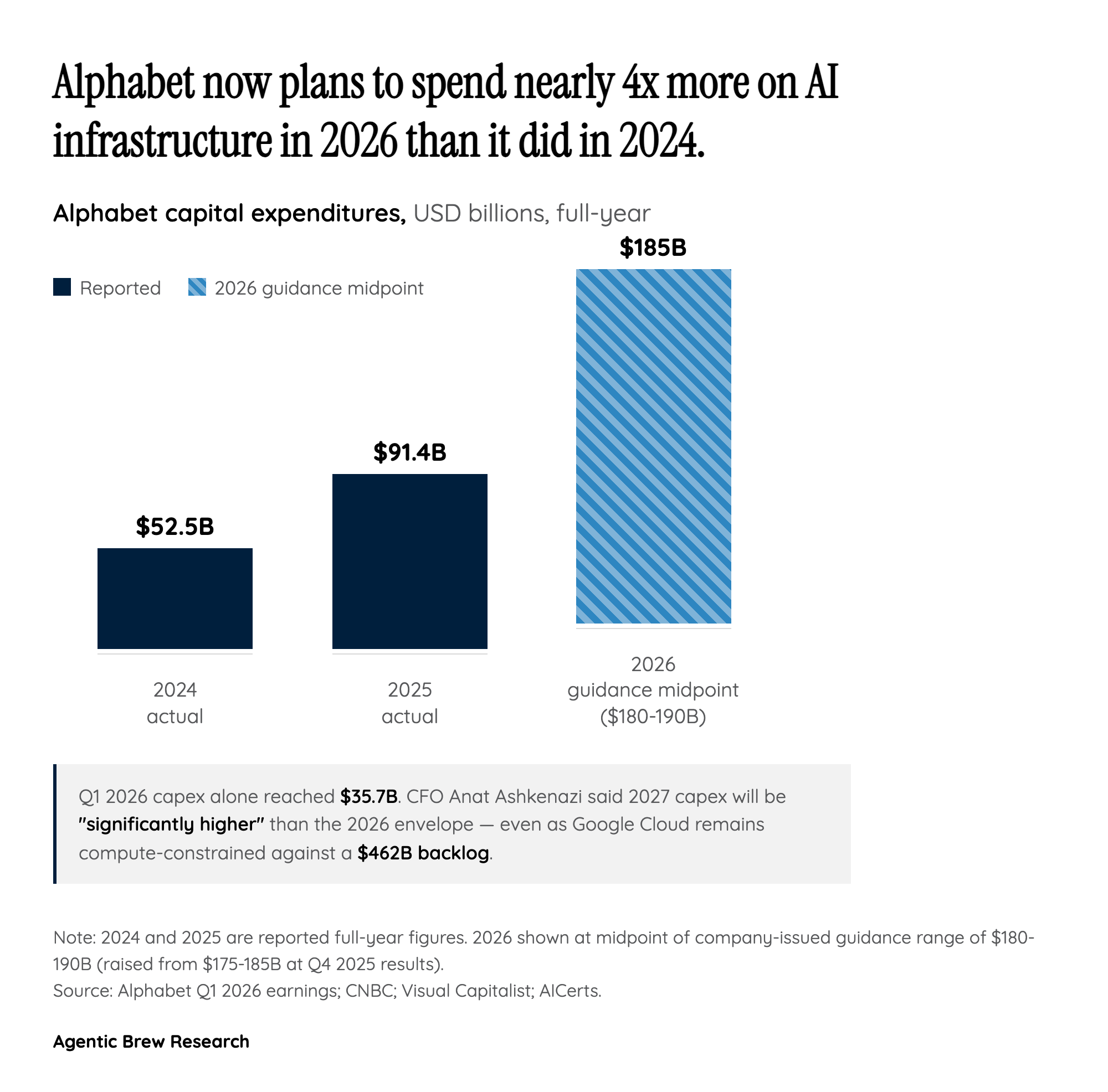

The clearest signal of the quarter wasn't Alphabet's $109.9B top line — it was the divergent stock reaction across hyperscalers that all raised capex on the same week. Alphabet jumped roughly 7% after-hours on a guide of $180-190B for 2026. Meta, which raised its own range to $125-145B, fell 6-7% and was promptly downgraded by JPMorgan to neutral over a 'challenging path' to AI returns. Microsoft, with $190B in guided capex, traded essentially flat. The differentiator is contracted demand: Alphabet can point to a $462B Google Cloud backlog and a 63% YoY cloud growth rate as the receivable side of its capital plan. Meta's AI build is funded by a single ad business and a hope that Llama and recommendation systems eventually drive enough engagement and ad pricing to clear the hurdle. Investors are no longer underwriting AI capex at the asset-class level — they're underwriting it issuer by issuer, and the presence or absence of a multi-year backlog is becoming the key discriminator.