Strategy followed physics: Azure simply ran out of room

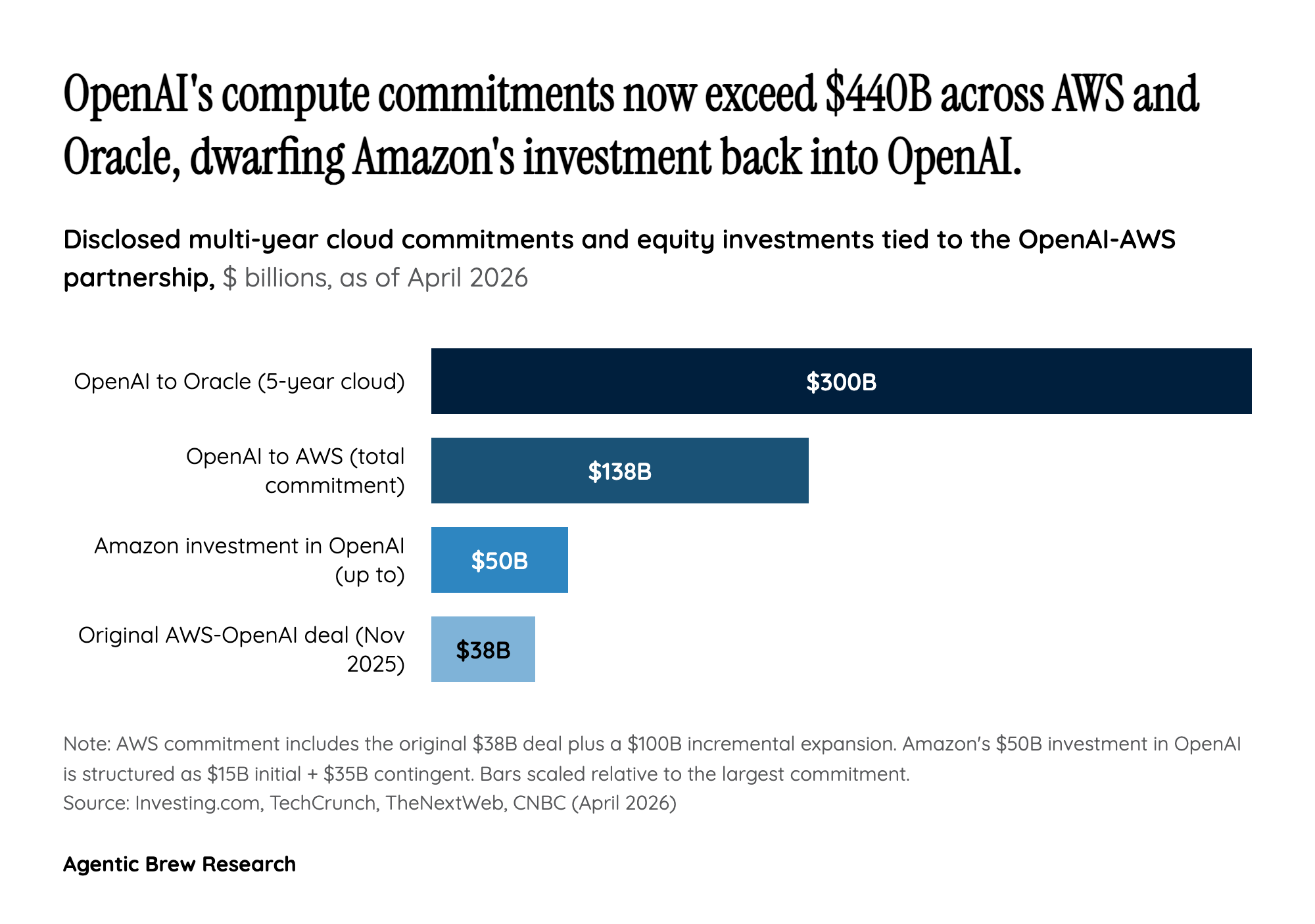

The official narrative casts the AWS deal as OpenAI choosing multi-cloud independence and Microsoft graciously letting go. The more grounded read, surfaced in community discussion on r/microsoft and r/singularity, is that the deal was forced by capacity, not strategy: Microsoft's data centers physically could not rack enough GPUs fast enough to satisfy OpenAI's compute appetite once the Stargate program, the $300B Oracle partnership, and an additional $138B AWS commitment were stacked on top of existing Azure consumption. Exclusivity is a luxury you can only afford if you can deliver the hardware.

This reframes the April 27 restructure from a competitive concession into a logistical settlement. Microsoft kept what it could defend — equity, an IP license through 2032, and a revenue-share stream from OpenAI — while giving up an exclusivity clause it could no longer operationally enforce. Read this way, AWS did not pry OpenAI loose; it absorbed the overflow, then formalized that role with the 'exclusive third-party cloud distribution' designation. The buried implication for the rest of the AI industry is that even hyperscaler-scale capex is now a binding constraint on frontier-model strategy, and contractual exclusivity with a single cloud has a short half-life when training-cluster demand is doubling year over year.