The 15-quarter high: what actually flipped at AWS

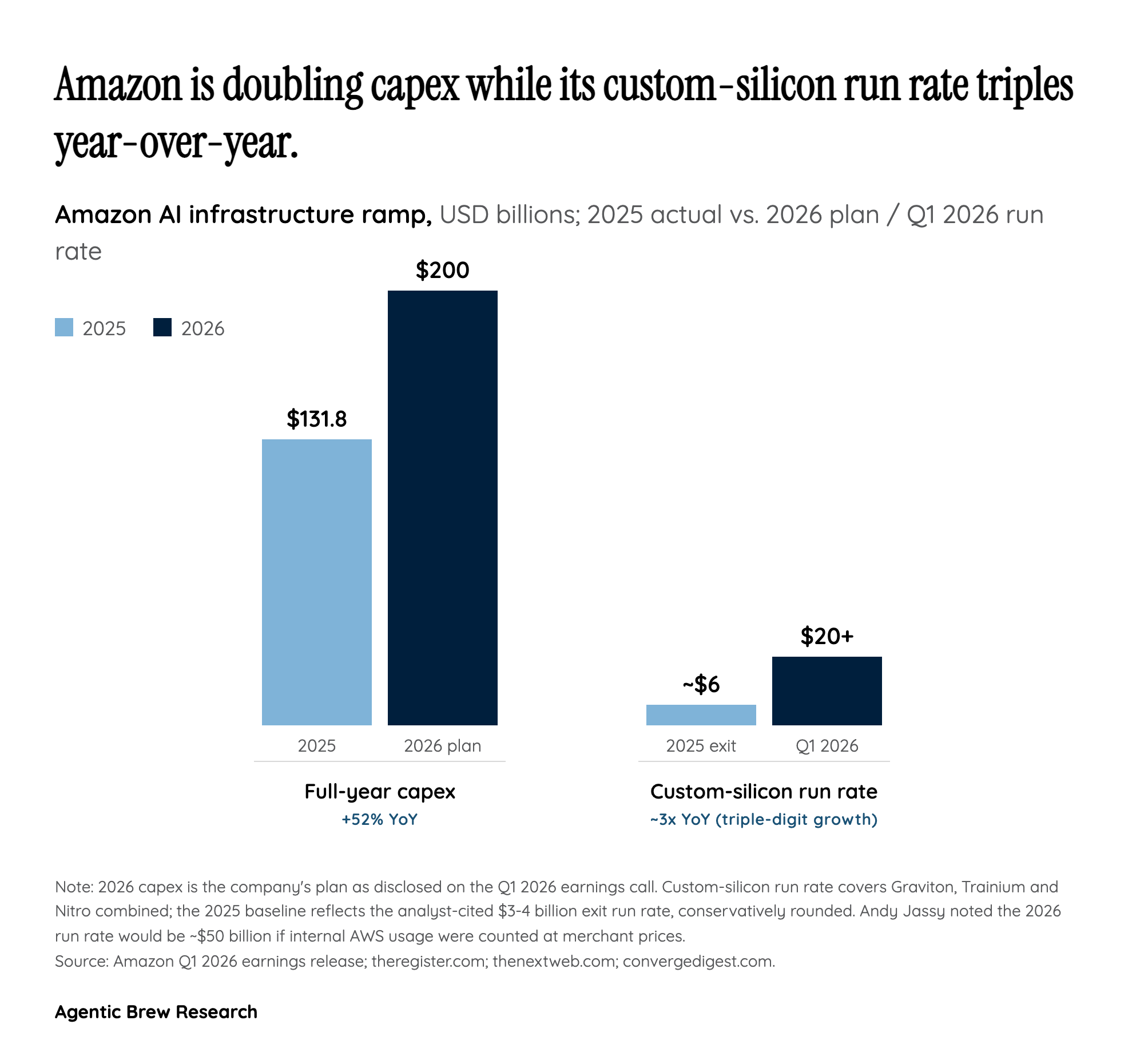

AWS's 28% Q1 2026 print is the segment's fastest growth pace since late 2022, and it landed on a base that has roughly tripled since then. The mechanical drivers Amazon disclosed are unusually concrete for an AI narrative: a $364B backlog (excluding the freshly signed $100B+ Anthropic deal), Bedrock customer spend up 170% quarter-over-quarter, and an AI revenue run rate above $15B. Bedrock processed more tokens in Q1 than in all prior years combined, suggesting the reacceleration is real workload throughput, not deferred-revenue accounting.

The second flip is competitive. For most of 2024-2025, AWS was the slowest-growing of the three big Western hyperscalers; this quarter, with Azure at 31% and Google Cloud at 28%, AWS is no longer the laggard on a percentage basis and is by far the largest in absolute dollars. Combine that with a 37.7% AWS operating margin and $14.2B of AWS operating income, and Amazon is doing something rivals are not — sustaining hyperscaler-grade margins while ramping AI capacity. The reacceleration is therefore better read as a vertical-integration dividend than as a one-quarter beat.